|

|

|

|

|

|

||

|

| AMC Speak |

5th March 2012 |

|||

| Enrich your financial solutions with this innovative proposition | ||||

| Ashok Kanawala, Head Business Development and Training, HDFC AMC | ||||

Value cost averaging (VCA) has many fans globally among financial planners and wealth managers, and is acknowledged as a very useful refinement of the good old rupee cost averaging (RCA) technique, which is at the heart of SIPs and STPs. Its utility gets enhanced in volatile market conditions, like we have been witnessing in recent years. Ashok Kanawala takes us through how VCA is different from RCA, how HDFC MF has utilized this concept in creating its new Swing STP and how you can use Swing STP to enrich the financial planning solutions you offer to your clients.

Value cost averaging (VCA) has many fans globally among financial planners and wealth managers, and is acknowledged as a very useful refinement of the good old rupee cost averaging (RCA) technique, which is at the heart of SIPs and STPs. Its utility gets enhanced in volatile market conditions, like we have been witnessing in recent years. Ashok Kanawala takes us through how VCA is different from RCA, how HDFC MF has utilized this concept in creating its new Swing STP and how you can use Swing STP to enrich the financial planning solutions you offer to your clients.

|

| |||

|

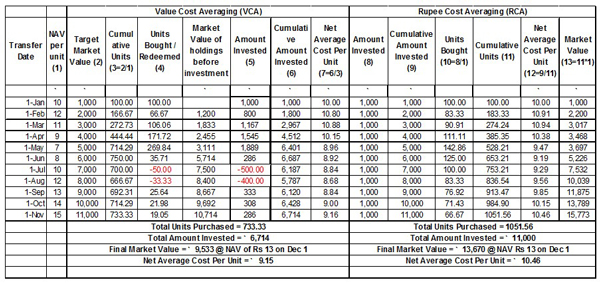

WF : In what ways is the Swing STP different from the normal STPs? Ashok : HDFC Swing Systematic Transfer Plan ("Swing STP") works on the principle of Value Cost Averaging (VCA) viz. invest more when NAVs are low and less when NAVs are high and draw the excess when the portfolio value exceeds the target value. Normal STPs work on the principle of rupee cost averaging which is to invest a fixed amount throughout the tenure of the STP irrespective of the market fluctuations. WF : Can you please take us briefly through the concept of Value Cost Averaging and explain how it's different from the Rupee Cost Averaging principle which is what is currently used in all STPs and SIPs? Ashok :The rule under Value Cost Averaging (VCA) is simple: make the value (not only number of units) of your portfolio go up by a fixed amount each month. The investor first sets a predetermined worth of the portfolio in each future time period. The investor then buys or sells sufficient units so that the target value is achieved on each transfer date. During periods of market decline, the investor is required to purchase relatively many units to maintain portfolio value. Conversely, during rising markets the technique requires the purchase of relatively few units or might even require that units be redeemed to maintain portfolio value at the desired level. Rupee cost averaging (RCA) on the other hand involves investing a fixed amount every month irrespective of portfolio value. Just like in RCA, in VCA more units are purchased when Net Asset Values (NAVs) of units are low. However, VCA requires that relatively more units are purchased as NAVs decline since the unit price decline reduces the value of the portfolio. Furthermore, and distinct from RCA, VCA also provides a rule for selling. As market price increases, VCA may require redemption of units since the rise in NAV increases the value of the portfolio over the target level. Thus, this helps to buy more at lower prices and sell at higher levels; helping to reach individual financial targets in a steady, progressive and less volatile manner. The following table is for illustration:

Disclaimer: This is just an illustration explaining the difference Value Cost Averaging & Rupee Cost Averaging using assumed figures. The above illustration is merely indicative in nature and should not be construed as an investment advice. It does not in any manner imply or suggest current or future performance of any HDFC Mutual Fund Scheme(s). WF : What are the advantages of using Value Cost Averaging over Rupee Cost Averaging? In what kind of market conditions would VCA deliver better results compared to RCA? Ashok : VCA has the following advantages over RCA:

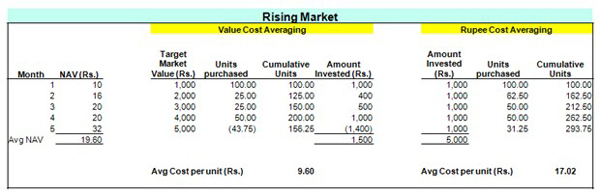

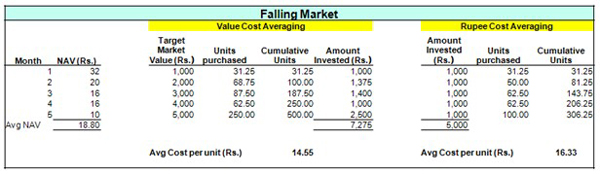

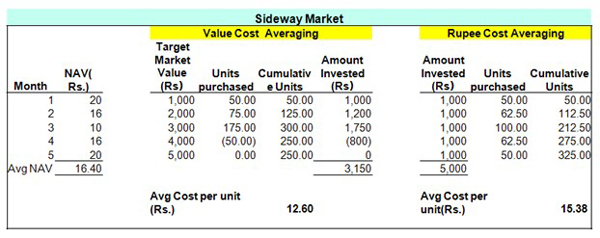

The following tables show how VCA fares against RCA in different market conditions:

Disclaimer: This is just an illustration explaining the difference Value Cost Averaging & Rupee Cost Averaging using assumed figures. The above illustration is merely indicative in nature and should not be construed as an investment advice. It does not in any manner imply or suggest current or future performance of any HDFC Mutual Fund Scheme(s). Under different market scenarios, VCA has lower average cost per unit as compared to RCA. RCA is an ideal strategy when an investor wants to invest a fixed amount till the end of the tenure irrespective of the market levels whereas VCA is an ideal strategy when the investor wants to invest a varied amount every month, depending upon the fluctuations in the market and arrive at a specific target portfolio value at the end of the tenure. WF : How will Swing STP actually work? Ashok : A unit holder has to decide the amount by which the portfolio value should appreciate at the end of each predetermined frequency say monthly. He needs to open an account in any of the debt schemes ("Transferor Scheme"). Thereafter he gives an instruction to transfer an amount to the growth option of the designated equity scheme ("Transferee Scheme") at predetermined frequency. On the Swing STP date, it shall compare the market value of the portfolio with its target value and transfer the difference. The total amount invested through Swing STP over its tenure in the Transferee Scheme, may be higher or lower than the Total Target Market Value of the investment. This may be on account of fluctuations in the market value of the Transferee Scheme. The following illustration will make the concept clear: Suppose you want the portfolio value to increase by Rs. 10,000 every month Money is transferred from a debt scheme to the growth option of a select equity scheme or vice versa i.e. reverse transfer using the formula: (First Installment Amount X No. of Installments including current installment of investments) minus (Market Value of the investments through Swing STP in the transferee scheme on the date of the transfer.) In case, Market Value is more than first installment X No. of installments including current installment, then redeem the excess units which are then invested into the Transferor Scheme which is termed as reverse transfer. On every Swing STP date, the amount transferred shall be higher or lower than Rs. 10,000 depending on fluctuation in market value of the equity scheme WF : If an investor does not want an automatic redemption when the portfolio value exceeds target value due to tax considerations, can he opt out of the auto redemption? Ashok : No. The auto redemption works on the principle of value cost averaging. However the unit holder has the option of discontinuing the Swing STP anytime during the tenure and within 15 days of the notice the Swing STP will be ceased. WF : In what ways can advisors incorporate Swing STP as part of their goal based solutions - especially when most of their clients may not have sufficient lump sum amounts available to set up these Swing STPs? Ashok : We suggest the following strategy from a financial planning point of view: Suppose an investor needs Rs. 6 lacs after 5 years for child's education viz. the value of the portfolio should appreciate by Rs. 10,000 p.m. However, the investor does not have enough lump sum amounts to deposit in the debt scheme towards his financial goal What is the solution? The investor can open an account in the debt scheme with an initial investment amount which is equal to say 5 to 6 times the amount he wants his portfolio to appreciate on a monthly basis viz. Rs. 50,000 to Rs. 60,000 Start SIP for e.g. on the 1st of every month into the debt scheme ,for an amount that is equal to value by which he wants the portfolio to increase in value on a monthly basis viz. Rs. 10,000 Register for Swing STP for e.g. on 5th of every month with an the first installment of Rs. 10,000 On every Swing STP, the amount shall be transferred from the debt scheme to equity scheme as per the formula specified Swing STP shall invest less when NAVs are high and more when NAVs are low and redeem the excess when portfolio value is more than target value and reinvest in the debt scheme Swing STP aims to ensure that you have the amount to meet your financial goal on termination of the Swing STP period (i.e. last swing STP transfer date) This is only a suggested strategy. Advisors are free to choose any alternative approach as a solution to the investor. HDFC Swing STP in any manner whatsoever is not an assurance or promise or guarantee on part of HDFC Mutual Fund/HDFC Asset Management Company Limited to the Unit holders in terms of returns or capital appreciation or minimization of loss of capital or otherwise. Mutual fund investments are subject to market risks, read all scheme related documents carefully. |

||||