|

|

|

|

|

|

||

|

| AMC Speak |

03rd July 2012 |

|||

| We are poised for a much needed upswing | ||||

| Tushar Pradhan, CIO, HSBC AMC | ||||

|

Tushar believes that after a 4 year long period of range bound activity, the Indian market may be poised for a much needed upswing - and he lays out his reasons for this optimism. Read on as he discusses the factors that have driven the relative outperformance of his HSBC India Opportunities Fund amidst turbulent times, his views on yesteryears darling sector - infrastructure and today's emerging hero - the banking sector and how big an issue are NPAs for this sector that is becoming an MF industry favourite. |

| |||

|

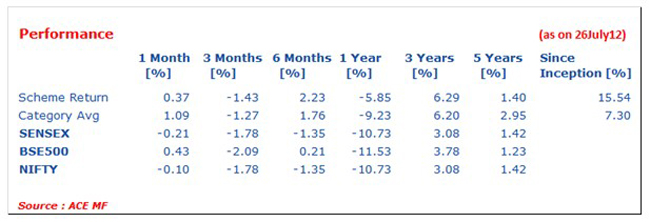

WF : Your HSBC India Opportunities Fund seems to have held up relatively better than market indices and category averages over the last 6 months and 1 year, amidst difficult market conditions. What are some of the strategies and calls that have helped performance in this period?

Tushar : Principally, HSBC Global Asset Management has moved towards a common, longer term philosophy based on profitability versus valuations, globally. While the description of the method is pretty intuitive, our research shows that a disciplined approach to buying companies that look attractive on this matrix provides significant longer term outperformance. However this is not a fool proof-all seasons strategy and there are times that companies that display attractive parameters based on the model may in fact, underperform the markets in short periods of time. This is due to investor preference to chase safety in relatively expensive but consumer stocks with better cash flow visibility in times of adversity or investor fancy on concept stocks that are highly expensive on the price to book matrix in the short term. We believe that our adherence to this framework has helped us identify stocks that have helped the performance of the fund over this period. WF : What are the sectors and themes that you are currently overweight on in this fund? Which are the key underweight sectors at this point of time and why? The fund today is overweight on auto and auto components, banking and financials and capital goods. Key underweights are household and personal products, pharmaceuticals and utilities. The framework as described above is favouring exposure to these sectors as valuations have become cheap following the slowdown in the economy. Investors prefer more expensive albeit defensive sectors presently which we believe offers an opportunity to gain significantly from a change in macro fundamentals and a return to "risk-on". While we do not know when this is likely to happen, investors are likely to be disappointed if they remain in expensive sectors as history does not provide a case when outsized returns are possible from expensive stocks on a perpetual basis. We of course are taking a balanced view of the same and have a diversified collection of stocks across the spectrum; however the drivers for outperformance will remain the sectors mentioned above. WF : What is the current market cap composition in this fund and how has this moved over the last 1 year? Tushar : As of now and in the manner how we classify large cap, we own a total of 66% in the large cap category and the rest in mid caps and cash equivalents. We have progressively increased our mid cap exposure over the past few months. WF : Are we looking at more earnings downgrades in the coming quarters or can we say that the worst of this cyclical downturn is hopefully behind us? Tushar : While it is always difficult to predict the end of a cycle, we believe the macro headwinds of high inflation, high interest rates and slowing rates of GDP growth point to things getting slightly worse before they change for the better. The problem with announcing the end of the downturn is that most indicators that show the same are "lagging indicators" and the market would have already anticipated the same, corrected significantly upward and then the numbers would follow. But the longer the downturn lasts, more is the confidence that the turn is just around the corner. WF : One of the biggest disappointments for investors and advisors alike is the continuing underperformance of the infrastructure sector. Is it reasonable to say that all the bad news is in the price and the outlook should now improve or should one brace oneself for a more prolonged period of underperformance? What is your portfolio stance on this theme - are you overweight cap goods and infrastructure now or underweight? Tushar : As mentioned above we are overweight capital goods vis-a-vis the benchmark; however we do not believe the infrastructure sector is fully out of the woods. The macro environment is still very cloudy and the biggest boost to such companies comes only when there is a significant macro angle to the story. With continued high interest rates, policy inconsistency and lack of promoter confidence at the moment, we do not think the fortunes of this sector may change soon. However from an investor's point of view who wants to take a 2-3 year view, this may seem to be an attractive sector to be in. We have taken selective exposure to capital goods sector that does not fully depend on the infrastructure sector alone but provides a balanced exposure to the turnaround in the economy as and when it happens. WF : The banking and financial services sector seems to be emerging a favourite among fund managers these days. What is your view on this sector? Is the risk of NPAs significant enough to be a key concern? Tushar : While we are overweight banks, it is for obvious reasons. Fearing a significant slowdown and deterioration in asset quality, stock prices have been beaten down. With a better than expected scenario, there could be a significant upside from current valuations. I suspect this is the reason most fund managers prefer to be in this space. However the risk of NPA's is not a small one. We believe the experience will not be uniform across the sector. As we have seen in the recent quarter gone by, some banks have weathered the storm better than others, and that provides us an opportunity to gain from the valuation differential as it emerges. WF : What is your overall market outlook for the next 12 months - are we likely to continue in the same range or do you see a breakout in either direction? What will be the key drivers for the Indian market over the next 12 months? Tushar : I believe after a period of range bound activity the Indian market is poised for a much needed upswing. I may be speaking more from hope than any real fundamental reason here, but the facts are compelling. The Indian market is trading at one of its lowest valuations as compared to its history. The earnings growth number seems reasonable and the time correction in the markets now has crossed the fourth year. With reasonable growth expectations and foreign interest, the market is capable of the upswing I am talking about. The risks of course remain and the same can be classified as 1. An external global event. 2. Domestic sluggishness persisting beyond the current financial year and/or 3. A breakdown of interest in India as an investment destination, for a while. Mutual fund investments are subject to market risks, read all scheme related documents carefully. The article is for general information only and does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this information. Investors should understand that statements made herein regarding future prospects may not be realised. The views expressed in the article are personal views of the author and do not necessarily reflect the views of HSBC Asset Management (India) Private Limited or any of its associates. Neither this document nor the units of HSBC Mutual Fund have been registered in any jurisdiction. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management (India) Private Limited. HSBC Asset Management (India) Private Limited; 16, V. N. Road, Fort, Mumbai 400 001. Tel: 6614 5000. Email: hsbcmf@hsbc.co.in. |

||||