|

WF: CY16 has been a fantastic year for you as a fund manager - all 4 of the funds you manage are top decile in their respective categories (Top 100 in Large Caps, Dynamic in diversifieds, and Balanced and Equity Income in their respective categories). Heartiest congratulations on this fantastic performance! What have been the winning strategies that have led such an impressive performance?

Naren: In fund management, our maximum focus is on process, over which we have complete control. What I have learnt over the years as a fund manager is that one should stay focused on the process and keep fine-tuning the gaps through learning and experiences in fund management; when managing other people's money.

On that basis, essentially we followed the same process over a period of time, which was to avoid costly sectors and to avoid sectors where the cycle was extended. We were underweight on sectors like Non-Banking Financial Companies, select Auto stocks and Cement whereas we were overweight on sectors like Power Utilities and Telecom. The process which we follow involves buying sectors, which are cheap and not under spotlight but appears to have a moderate outlook.

You will be surprised to know that sectors like Utilities and Metals, which we were also positive in 2015, delivered reasonable returns. We will continue to follow our model of having a stable logical process for long-term performance. At the same time, while delivering this long term performance, there may be instances of short term volatility. Therefore, we will stick to our process because we have seen that process can leads to long-term gains for the investors.

WF: It is said that every successful fund manager develops and is guided by his/her own set of strong convictions/beliefs, and it is this conviction that enables them to ride out rough patches. What are the beliefs/convictions that shape your thinking on markets, on stocks, on investment opportunities?

Naren: My belief has been that one should follow a contrarian, value oriented, top down and bottom up style of investing. This combination has helped me to ride out rough patches as and when they occurred. For example in 2007-2009 cycle, there was a rough patch in 2007 which got stable in 2009 by following a process built on contrarian, value oriented, top down and bottom up style of investing. Over the market cycle such a style is likely to give a better outperformance. The style has been over a period of time, fine-tuned based on the experiences of eminent fund managers in the western world and the readings that they have managed to communicate to people like us through internet as a medium.

Wizards of Dalal Street

Part 1: https://www.youtube.com/watch?v=_2P3b8qBhxs

Part 2: https://www.youtube.com/watch?v=T9JyXFk3Hak

Part 3: https://www.youtube.com/watch?v=KHbsCk44qMc

WF: When you look back at your illustrious career as a fund manager and stock picker, what have been in your view your biggest wins? Is there a common thread that seems to run through either the kind of stocks that make this list or the circumstances they were in, when you picked them?

Naren: It is generally perceived that it is difficult to make money through value investing in a growth market like India. My biggest win has been the belief that value investing is not dependent on whether it is a growth market or not, but it is dependent on a steady application of the contrarian value philosophy in a systematic manner through market cycles. This is very important because value oriented contrarian approach is not capable of delivering in all parts of the cycle but once you systematically run such an approach you are likely to generate alpha over different market cycle.

WF: Who are the investment gurus whose wisdom and actions have materially shaped your thinking and your own investment philosophy?

Naren: James Montier, Howard Marks and Michael Mauboussin are the three investment gurus I follow. From Montier, I learnt the rules that can help pick stocks that can give spectacular returns in the long term. Marks taught that investing is common sense and what is important is controlling one's emotions as an investor. And finally, Mauboussin showed - assume what is likely to happen and act accordingly to reduce mistakes.

Q5 Looking back at the market from the liberalisation days of 1991 to today, what have been the biggest lessons that Mr.Market has taught you and how have you captured these lessons in shaping your investment philosophy?

Naren: Market has taught us that there will be bubbles. This year there was a fixed income bubble, which culminated into two European companies managing to borrow long term money at negative interest rates. So despite of sophisticated financial markets in the western world, you can find that periodically you will have bubbles and busts. The opportunities such bubbles and bursts would give to a fund manager are significant, once you ride out the psychological pain of handling the bubble or the bust.

Q6 It is said that the fiercely competitive market place, where the last 12 month returns materially impact fund flows, is a minefield for equity fund managers, which forces them to often align with market wisdom rather than personal convictions, in an effort to remain in the game of short term performance. How true is this? How do you manage to strike a balance between your own convictions and the dictates of the market place?

Naren: Having been a fund manager for twelve years, and having managed other people's money through the mutual funds system for a long period of time, we have managed to stick to a standard process at ICICI Prudential Mutual Fund. At times this has negative implications on short-term performance but having conviction in the process and staying with it in a stable way has able to generate long-term performance. This has been the experience with most of the mutual fund managers across the globe. Their good experience in the world markets over decades has helped us to shape our conviction.

CNBC Unplugged

Part 1 https://www.youtube.com/watch?v=U5_o9Vo49X4

Part 2 https://www.youtube.com/watch?v=VySOXudKGpQ

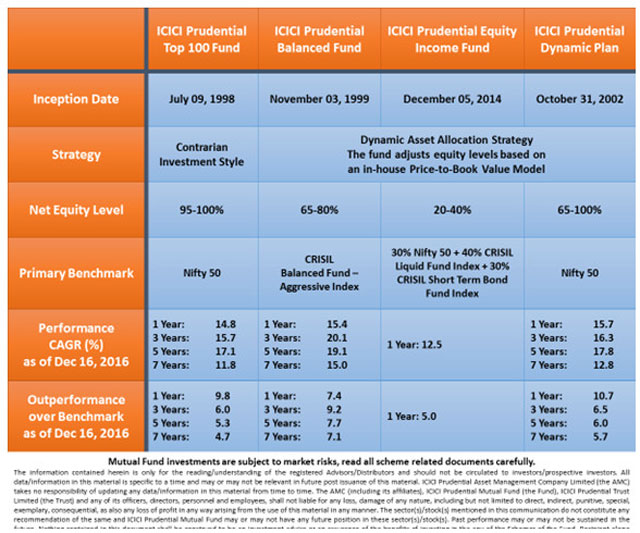

WF: What would you say is the common thread that runs between the 4 funds that you personally manage - Top 100, Dynamic, Balanced and Equity Income? Conversely, how do you try to differentiate their portfolios and their strategies?

Naren: The common thread that runs between the funds that I manage is the contrarian value oriented top down and bottom up theme. However, each of the portfolios has been different. For example in ICICI Prudential Top 100 Fund, we have a restriction on the amount of midcaps we can allocate to, in ICICI Prudential Dynamic Plan, we have an ability to take cash calls, in ICICI Prudential Balanced fund we run with a 65-80% equity exposure based on Price to Book Value model and in ICICI Prudential Equity Income Fund, the net equity exposure is between 20% to 40%. So each of the four schemes satisfy different customer base with different risk return expectation.

There seems to be growing concern that demonetization may leave an adverse impact on corporate earnings longer than initially anticipated. There is also some concern that GST implementation may bring some initial pain before long-term benefits kick in. Are we therefore looking at a further extension of the long saga of weak corporate earnings? Are market valuations adequately factoring in the near and medium term concerns?

Naren: We believe that Demonetization can be positive for corporate earnings and equity markets in the long run, be it with short-term volatility. We see this as an opportunity to increase equity allocation in a country where there are many people with underweight stance on equities. So we view the current weak corporate earnings as an opportunity to increase equity assets and believe that it is increasing the potential for Indian investors to make money in equities, courtesy the short-term weakness in corporate earnings and with a view to benefit from long term corporate earnings.

The fact that land, labor and capital have all become inexpensive with the potential that there is a likely leveraging cycle over the next two years means that the scope for equity market is better now post demonetization than pre demonetization, albeit with more volatility only in the near term.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

The information contained herein is only for the reading/understanding of the registered Advisors/Distributors and should not be circulated to investors/prospective investors. All data/information in this material is specific to a time and may or may not be relevant in future post issuance of this material. ICICI Prudential Asset Management Company Limited (the AMC) takes no responsibility of updating any data/information in this material from time to time. The AMC (including its affiliates), ICICI Prudential Mutual Fund (the Fund), ICICI Prudential Trust Limited (the Trust) and any of its officers, directors, personnel and employees, shall not liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. The sector(s)/stock(s) mentioned in this communication do not constitute any recommendation of the same and ICICI Prudential Mutual Fund may or may not have any future position in these sector(s)/stock(s). Past performance may or may not be sustained in the future. Nothing contained in this document shall be construed to be an investment advise or an assurance of the benefits of investing in the any of the Schemes of the Fund. Recipient alone shall be fully responsible for any decision taken on the basis of this document.

Share this article

|

AMC Speak

AMC Speak