|

Business sentiment is now perhaps lower than market sentiment

We finished a very tough year in the Indian environment. 2013 March ending if you take a rough poll within Corporate India on how business has shaped up, I think it actually has deteriorated towards the end of the last six months. After a very long time in Corporate India profits have grown virtually flat . What had helped overall Corporate India to maintain profitability and grow in the past few years was a reasonably significant rebound in the consumer spend and strong momentum in exports that had actually helped this economy sail through. The current environment has deteriorated, with an all time high fiscal deficit, a high social sector spending and elections around the corner.

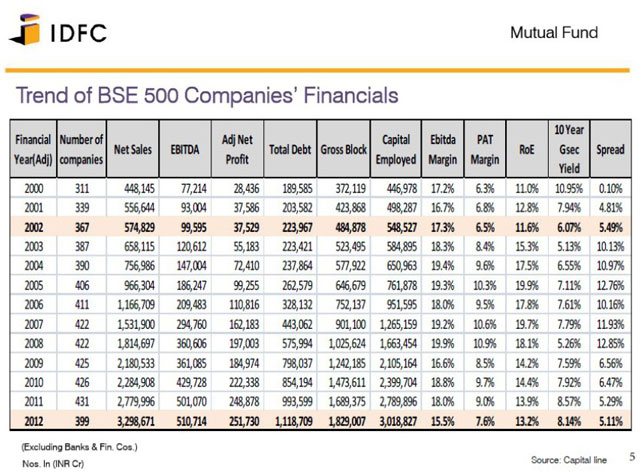

Key macro numbers are as bad as they were a decade ago

If you step back into the last decade when the emergence of the investment economy started off, the GDP went up from 5% to 9%, and today from a GDP context we are back at 5%. From a fiscal deficit context we are back at its all-time high. From a current account deficit we still need exports to kick in quite sharply to correct the balance of trade. So this is a macro-environment where we have virtually gone back to year 2000 which was the end of the first investment cycle. We are at a decade low ROE and PAT margin - as the data table below clearly demonstrates. We think that incrementally to grow profits from here, corporate India does not need to invest in anything, there is enough capacity on the ground which needs to turn profitable.

Businesses that handle this environment are likely to be tomorrow's winners

We believe in such an environment what also comes through is that companies that have been able to handle the pressures of a bad market can do extremely well in a market which is expected to recover, going forward. So the focus incrementally is on putting together a portfolio of companies that can come out at the top.

Strong, small businesses are perhaps where the best opportunities lie today

There can be many segments of companies that can potentially capture these opportunities. There's one that however looks very interesting at this point in time - small, yet stable companies across industries. To go back into history anything that started off in 2002 was completely non-descript and nobody had heard anything called the investment cycle then and this turned out to be a significantly large environment into 2007. So construction companies, cement companies, power companies, utilities, public sector banks which never ever participated historically actually participated with the environment into 2007 and 2008. And that is a window of opportunity that we see in 2013 into 2017. There will be a bulk of these companies that will be at the formative stage which we currently do not have on the radar but we would want to bring it into the fold. They might belong to niches but the niches will eventually grow up into an industry itself.

Why do we say the opportunity is back after a decade?

RoE and PAT margins are today where we last saw them 10 years ago - in 2002 - just before the last cycle started in 2003. The next market upmove from 2003 to 2008 was driven by small companies. They also fell the most in the subsequent period from 2008 to 2012 - such is the nature of this segment. We believe this fall has created an opportunity that was perhaps seen only a decade ago. The BSE Small Cap index is trading at 47% below its all time high while the Nifty is barely 6% off its peak. As the interest rate cycle continues turning, smaller companies are likely to benefit incrementally the most and first, which can set the scene for PAT margins to bounce back from their decade lows.

A vehicle to harness this opportunity: IDFC Equity Opportunity - Series I

That's really the idea behind IDFC Equity Opportunity - Series I, we have packaged it in a close ended format which would give us visibility of funds with a limited size of corpus that we are looking at mobilizing.

Fund will have a diversified portfolio of 60-80 stocks. The key for diversification is to manage liquidity/risk considerations and play across sectors. -

The guiding principle for building the portfolio will be:

Companies which are in existence for a long period of time with good track record Companies with stable promoters Companies with low to moderate leverage Companies which allocate capital efficiently

Stocks which are available at discounted valuations Fund will be a 3 year close ended fund. Fund will be by and large a buy and hold strategy

Risk to this strategy

Key specifications:

NFO Opens on 9th Apr 2013 and closes on 10th Apr 2013 can be extended if target corpus is not raised. Min Investment Amount - 5,000

|