|

Australian cricketer-turned-commentator Dean Jones, in an interview1 for Wisden,

observed that two-thirds of Sachin Tendulkar's game is based around defence. Most

of the shots in any Sachin century, he says, are based on forward defence, back-foot

defence and letting the ball go. As any coach would vouch, letting the ball go is

possibly as important as hitting good shots in the career of a batsman. In this edition

of Connecting the Dots, with analogies from the world of sports, we discuss why

inaction is just as important a strategy in the world of investing as action.

In the investing world there are huge incentives to make correct decisions. No

wonder it attracts among the smartest and brightest people who are well versed

with the most complex statistical and valuation models. The modern 'information

economy' is constantly throwing out gigabytes of data, coaxing the receiver of

this information to react. The institutional imperative for professional investors as

recipients of the information stimuli is typically to react by trading in the markets.

Over the years automation and algorithms have significantly made it easier and

faster to execute trades. The outcome of all this is a market where sell side analysts,

incentivised by the number of right calls they make, are constantly nudging their buy

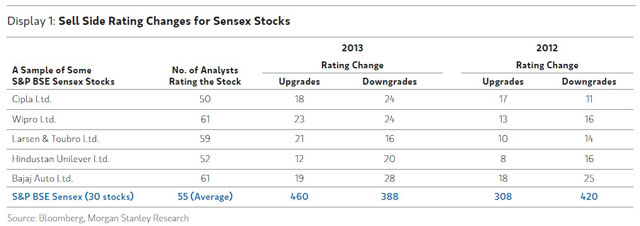

side clients to trade. For the thirty stocks in the popular S&P BSE Sensex index, the

average research coverage per stock is 55 analysts. Between them, they made as many

as 848 cumulative rating changes (either an upgrade or a downgrade in the research

recommendation) in 2013. As an example, take Cipla, a leading healthcare stock,

which is covered by 50 sell side research analysts. It had 42 rating changes during

the year 2013. In short, a portfolio manager would have received 42 calls to act on

(buy or sell) Cipla in one year (Display 1). The buy side managers succumb to the noise

generated from various quarters, forgetting that bigger contributors to portfolio returns

are factors such as bet sizes (portfolio construction) and the magnitude of returns generated

therefrom rather than the frequency of right calls in the market. This is reflected in higher

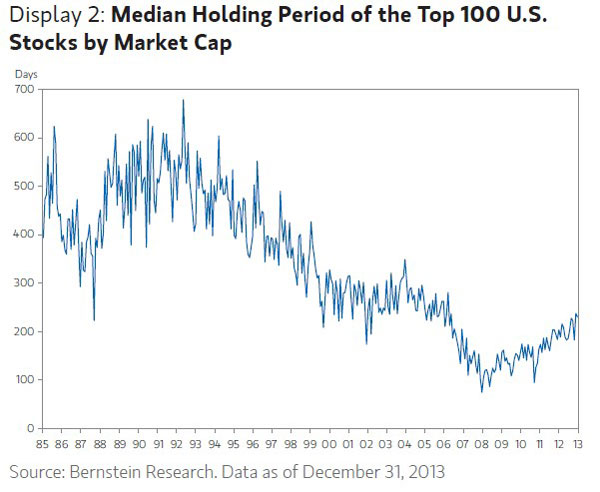

portfolio churn ratios, or in other words, shorter holding period of stocks in the portfolio.

In fact, the median holding period of the top 100 stocks by market capitalisation in the U.S.

has shrunk to a third from about 600 days to 200 days over the last two decades (Display 2).

Behavioural science uses the term action bias to explain such behaviour.

Action bias is the tendency in uncertain circumstances to choose action over inaction, no matter how

counterproductive it might be. It is the strong urge to act, despite the fact that an objective analysis

of past action might repeatedly prove that the action did not produce the desired results.

In an interesting research paper, Michael Bar-Eli2 et al analysed

286 penalty kicks in top soccer leagues and championships worldwide. In a penalty kick, the ball takes approximately

0.2 seconds to reach the goal leaving no time for the goalkeeper to clearly see the direction the ball is kicked.

He has to decide whether to jump to one of the sides or to stay in the centre at about the same time as the kicker

chooses where to direct the ball. About 80% of penalty kicks resulted in a goal being scored, which emphasises

the importance a penalty kick has to determine the outcome of a game. Interestingly, the data revealed that the

optimal strategy for the goalkeeper is to stay in the centre of the goal. However, almost always they jumped left or right.

The goalkeepers choose action (jumping to one of the sides) rather than inaction (staying in the centre).

If the goalkeeper stays in the centre and a goal is scored, it looks as if he did not do anything to stop the ball.

The goalkeeper clearly feels lesser regret, and risk to his career, if he jumps on either side, even though it may

result in a goal being scored.

Just like the goalkeeper, an investment professional too feels compelled to play every

trade that is out there in the market. In most cases either the event is already priced in or it just does not play out

in line with the popular belief. Despite data proving that frequent trading might be counterproductive,

the norm is always to act. Action seems to always triumph inaction.

So the next time you feel compelled to place a trade in the market, remember sitting

around and doing nothing may just be a better option. After all as Warren Buffett says, benign neglect, bordering on sloth,

remains the hallmark of his investment process.

Index Definition:

The S&P BSE SENSEX is a free-float market-weighted stock market index of 30 well-established

and financially sound companies listed on the Bombay Stock Exchange.

Important Disclosures:

As a part of Compliance disclosure, Amay Hattangadi and Swanand Kelkar hereby declare that as of today,

[including our related accounts] we do not have any personal positions in the securities mentioned above. However, one or more Funds

managed by Morgan Stanley Investment Management Private Limited may have positions in some of the securities mentioned in the missive.

The opinions expressed in the articles and reports on the website are those of the authors as of the

time of publication. We have not undertaken, and will not undertake, any duty to update the information contained above or otherwise

advise you of changes in our opinion or in the research or information. It is not an offer to buy or sell any security/instrument or

to participate in any trading strategy. The value of and income from your investments may vary because of changes in interest rates,

foreign exchange rates, default rates, securities/instruments prices, market indexes, operational or financial conditions of companies

or other factors. Past performance is not necessarily a guide to future performance.

Investors are advised to independently evaluate particular investments and strategies, and are

encouraged to seek the advice of a financial adviser before investing.

It is not possible to invest directly in an index.

Charts and graphs are provided for illustrative purposes only.

1Kids need to be taught the art of defence. Retrieved Jan. 31, 2014 from http://www.wisdenindia.com/

interview/kids-need-to-be-taught-the-art-of-defence-dean-jones/21682

2Bar-Eli, Michael and Azar, Ofer H. and Ritov, Ilana and Keidar-Levin,

Yael and Schein, Galit (2005). Action bias among elite soccer goalkeepers:

The case of penalty kicks. Retrieved Jan. 31, 2014, from http://mpra.ub.uni-muenchen.de/4477/

© 2013 Morgan Stanley

Share this article

|