|

|

|

|

||

|

|

| Advisor Speak |

03rd May 2012 |

|||

| Sell 140 SIPs and become a crorepati | ||||

| Jignesh V Shah, Surat | ||||

|

As the head of the South Gujarat IFA Association, Jigneshbhai is a worried man. As he looks around himself, he sees fellow distributors in a defeatist and negative mode - shoulders drooping, low on confidence, quick to complain about the challenging environment and constantly talking about moving out of MF distribution, into hopefully greener pastures. After 10 years in the MF distribution business, Jigneshbhai is completely convinced that this is the best business to be in - despite the huge challenges that IFAs are facing.

|

||||

|

Career Options Since there is a lot of discussion on an alternative line to MF distribution, it makes sense to start from the basics and evaluate all options that we have in front of us. There are 3 basic career options that each of us have :

1. Take up a job Here is how I see the benefits and concerns of this option : Benefits: - Steady Income - Regular Rise In Income - Less Risky Concerns: - Higher Education Required - It Pays You Well Till Health Permits - Limited Growth - Influence & In Some Cases Bribing Required - YOU WORK FOR SOMEONE ELSE

2. Become a professional When We Talk About Professional; We Are Referring To Doctors, Advocates, CAs etc. This is how I see the benefits and concerns of this option : Benefits: - Gives You Respect - Pays You Handsomely If You Are Successful Concerns: - Costly Professional Degree - Experience Required - Investments In Workplace, Employees, Technology required. - Requirement of Constant Working Capital - Time Consuming & May Not Get Immediate Success - Need To Charge & Collect Fees 3. Run your business These are the pros and cons in my view of running your own business : Benefits: - Sky Is The Limit - Huge Income - Gives Money/Status/Fame etc.. Concerns: - 95% of Start Up Businesses Fail In First 3 Years - High Investment Value - Family Background/Mentor is Necessary - High Risk & Huge Capital Requirement - Payments Are Untimely & Difficult Sometimes, Requires many Man-hours - Probable Government/Bureaucratic Harassment - Cyclic In Nature [Bear & Bull] Between becoming a professional and running your business, the choice is clearly dependent on your own aptitude, skills and interests. Some of us like higher education and want to acquire professional qualifications like CA etc, while others may prefer to start a business and learn and grow through real life experience.

MF Distribution as a business Now, lets look at MF distribution as a business option. Right now, most of us can think of a long list of negatives with this business, which can be summarised as follows : Concerns: - Low Immediate Income - Constant Knowledge/Updation Required - Very Fast Regulatory Changes - Requires Lot of Field Work - Market Linked Volatility - Confusion Due To Variety of Products Availability - Lack of Value For Advisor Are there any benefits at all in this business? If you think about it carefully, you will realise that in each of these concerns, lies a benefit for you - its only a question of how you look at it - your attitude towards challenges : Concerns - or benefits? - Low Immediate Income; Yet Huge Future Income Via Power of Trail. - Constant Knowledge/Updation Required; Which Makes You An Informed Person. - Very Fast Regulatory Changes; Makes Your Business Convenient, Transparent & Responsibility Free. - Requires Lot of Field Work; Gives You An Opportunity To Meet Different People. - Market Linked Volatility; Gives You An Opportunity To Grow Your Business. - Confusion Due To Variety of Products Availability - Better Options. - Low Acceptability By Investor - Huge Scope In Future. - Lack of Value For Advisor - Create Your Value & Importance Its not just an attitude change that we need. There are some major plus points of MF distribution that we ignore in this mood of negativity :

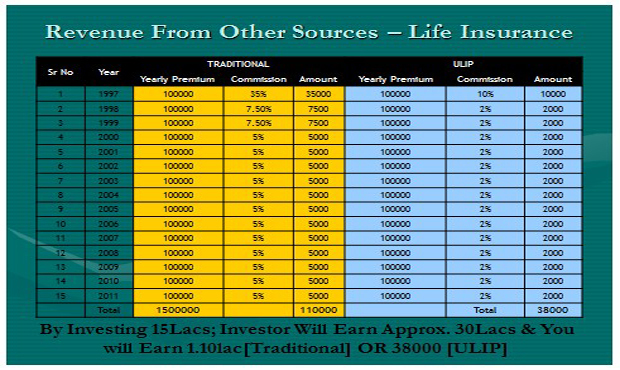

Lack of investor awareness - a weakness or strength? One of our biggest challenges is that investor awareness of mutual funds is still very low in our country and that makes selling MFs a big challenge. My favourite story for this is the famous story of the two shoe salesmen in Africa. Two shoe salesmen were sent to Africa to see if there was a market for their product. The first salesman reported back, "This is a terrible business opportunity, no-one wears shoes." The second salesman reported back, "This is a fantastic business opportunity, no-one wears shoes." The only question that I have is, when confronted with a problem or challenge, which salesman are you? Surat's bank deposit base is Rs. 35,000 crores and mutual fund AuM is around Rs. 4000 crores. Should you focus on the size of the potential or the present low penetration? Do you really make more money selling insurance and bonds than MFs? The other big challenge that we constantly discuss is that ever since loads went away, distribution margins in mutual funds have become unattractive. Many of us have started focussing more on insurance and bonds, because they pay us more. Is that really true? Lets take a typical case of an investor investing Rs. 1 lakh per year for 15 years. First, lets take a typical traditional life insurance policy.

If you look at the last 15 years track record, your investor's Rs. 15 lakh (1 lakh per year) would have fetched him Rs. 30 lakh at the end of 15 years. You would have earned about Rs. 110,000 from these investments of your client.

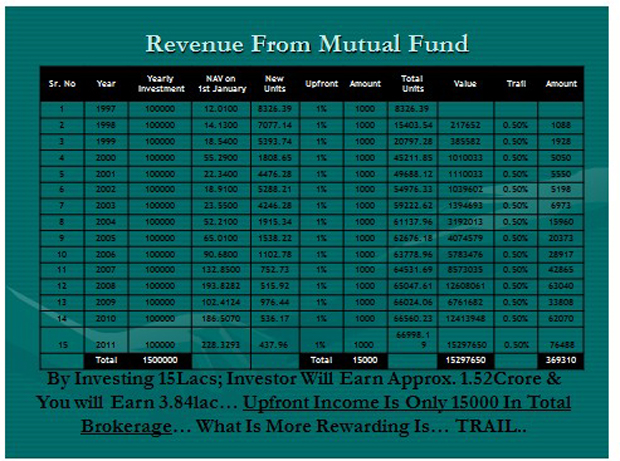

The same Rs. 1 lakh per annum invested in equity funds would have meant that your client's investment value reached Rs. 1.52 crores at the end of 15 years (as opposed to Rs. 30 lakh in a life insurance policy) and your earnings over this period would have been Rs. 3.84 lakhs (as against Rs. 1.10 lakhs) - assuming a 1% upfront and 0.5% trail. The bigger issue we need to remember is that out of this Rs. 3.84 lakhs, as much as Rs. 3.69 lakhs would have come by way of trail and only Rs. 15,000 by way of upfront. I fail to understand why so many distributors keep focussing on upfront commission, while the real earnings in this business is from trail - as this example clearly shows. Now, lets look at the other distributor favourite : traditional debt instruments like NSC, company deposits etc.

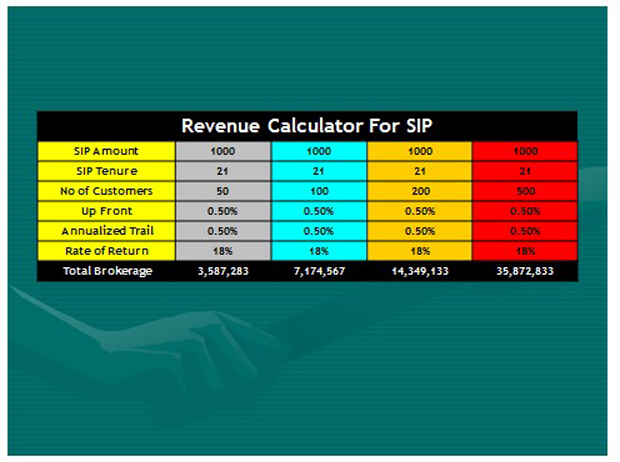

Most mutual funds in the debt and liquid plus segments give you a brokerage of 50 paise a year. You earn more money from debt and liquid funds, and your clients enjoy better post-tax returns as well. Clearly, you will offer your clients products that are best suited to their needs - whether it is mutual funds, insurance or bonds. But the point is that if you choose as a businessman to migrate away from mutual funds towards insurance and bonds in the belief that you will earn more money there, you need to look at the facts again and then decide for yourself. Sell 140 SIPs and you can become a CROREPATI If you simply focus on selling long term SIPs, you can build a very profitable business. Just like you do long term projections of wealth creation for your clients, do one for yourself and you will see the power of trail income via SIPs. Every 140 SIPs that you sell will earn you over 1 crore rupees in trail income !

This table above shows that if you get 200 clients to set up long term SIPs of 21 years of even small amounts like Rs. 1000 per month, at 0.5% upfront and 0.5% trail and with a CAGR return of 18% over the next 21 years, your income will be Rs. 1.43 crores! If you get 500 such SIP clients, your earnings will be Rs. 3.58 crores! Some people have questioned me on the 18% return assumption - they think it is on the higher side. My only response is that this shows lack of conviction in long term equity returns, because of short term market challenges. Equity funds have delivered those kind of returns in the last 20 years and I see no reason why the next 20 years will not be better for our country and therefore for equity markets. However, for your own working, you can assume a lower return figure - say 15% and see for yourself how many SIPs you need to sell for every 1 crore of commission income you want to create for yourself. My target is 140 SIPs = 1 crore commission, somebody else can say 200 SIPs = 1 crore commission. The basic point is to understand the power of creating wealth for yourself from a simple business model of selling long term SIPs. Technology and technical skills are not barriers in this business Of late, I hear many people say that if you are not technologically savvy, you have no future in this business, because the whole business will go into online platforms etc. That frightens many of us who are not that tech savvy. Then there are others who say technical skills and deep market insights are necessary to be successful in this business - which again puts some distributors on the back foot. My take is very different - this is a very simple business, which can be done by all of us, so long as we think first of our clients and then about our income. Technology platforms, technical skills etc are no doubt very good - but if you are not comfortable with that, you can still run a very successful business. Trust and confidence of your clients is earned by thinking about them first and about yourself next. Winning your clients trust and confidence is what is needed for you to attract more clients. All you need to do really is to pass the AMFI exams, understand your products, their risks and their benefits, and explain this with conviction to your clients. Today, many AMCs are conducting regular training programs on various aspects that help us do our business better - attending all these programs is enough to keep you fully aware of what you need to know in this business. There is no need to fear technology - if you are reluctant to embrace it, that doesn't mean you can't run a mutual fund distribution business successfully. To conclude Gandhiji said "Customer is GOD". Just embrace that philosophy. Do what is right for your customer and you will undoubtedly succeed. If that is your philosophy, you will realise that mutual funds are the best vehicle to make money for your clients and for yourself. There is a huge need for investors in India to be made aware of the virtues of mutual funds - that is what our single focus should be. And, if we keep that focus always in mind, we can build very successful businesses for ourselves. Just keep remembering : every 140 long term SIPs you sell, can make you 1 crore in commission income ! |

||||