|

WF: What is the Smart Asset Allocation product that you are launching and how will it work?

Srikanth: It is a Wealth Management solution that brings together the best of research, advice & execution, all in one place. It is offered through a PMS of Mutual funds and has three schemes to suit 3 Risk profiles - Balanced, Moderately Aggressive & Aggressive that can suit their client's financial plan and asset allocation needs.

E-SAAS is designed to take over the ongoing burdens of an advisor in implementing a financial plan over a life time of one's relationship with their client. All that an advisor needs to do in this arrangement, is help the client open a PMS account, select the scheme suitable to the client and arrange for a single check/fund transfer. Thereafter, the well-designed process begins its support to the advisor, in terms of operationalising the investments and redemptions that help in tactical asset allocation required to stay ahead of the markets and expectations

WF: What are the parameters that go into your asset allocation model? How does back testing of your model stack up? How is it materially different from some of the models embedded into popular funds?

Srikanth: C-TAAf (Citadelle - Tactical Asset Allocation Framework) our proprietary tactical asset allocation model is designed to help advisors stay ahead of sizeable market turbulences that affects all risk assets similarly in the short term. This happens when prevailing fundamental strength is increasingly disconnected from sentiments around it. To identify the opportune moments to continue to take risks or avoid it, C-TAAf considers the combined strength of four key variables like earnings momentum, fund flows, under/over valuations and its persistency. Our models` back tested results, help us strongly conclude that to maximise ones` returns, one is better off managing acceptable risk than taking on extra risks.

C-TAAf is different in its applicability to advisors. C-TAAf is an advisor oriented multi-factor model that facilitates the application of tactical asset allocation at an overall portfolio level of a client which are many. For example were C-TAAf to guide a risk-off phase, the advisor can use it to minimise risk by allocating to cash funds or stop allocating further money to risk assets or simply redeem existing investments apart from considering long-short funds to maximise the risk off phase. On the contrary when C-TAAf signals taking risks, one can deliver greater alpha by going into mid-caps & small caps from among many choices of funds. The advisor can further fine tune the quantum of allocation & dis-allocation to suit his sense of different risk profiles. This is unlike models embedded in a fund which restricts its applicability beyond the limited allocation made to it.

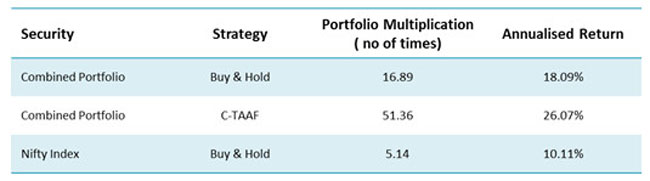

Let me illustrate the C-TAAfs effectiveness through the back-tested results from Jan 2000 and its live performance since 2015.

Let's consider of a buy & hold 50:50 portfolio of a flexi-cap fund like HDFC top 200 and a mid-cap fund like Franklin India Prima, held since 2000 Jan. Let us now contrast this with the same portfolio that builds tactical asset allocation into it, by way of raising cash partially ( say by 30%) when indicated to do so by C-TAAf. The results do inspire comfort & confidence

Results for a Tactical Asset Allocation based on sample P/E triggers of 18 & 22, and 30% exit are as below

The Wealth Multiplication difference between the Index and the C-TAAf based portfolio is the source of Advisory Value Add by an advisor and one that deserves respect & advisory fees from clients. Our portfolio reporting systems go the extra length to illustrate it in an interactive manner such that the Advisory Value Add is beyond dispute.

WF: What is the key benefit for IFAs and for their investors in this proposition?

Srikanth: Benefits for IFAs

a. Convenience in engaging and serving clients

b. Equal attention to all clients` in terms of portfolio construction & simultaneous execution

c. Substantial savings in operational time & co-ordination and its opportunity cost

d. Scalability of their business by redirecting the saved time, for two critical activities that actually grow the business - client acquisition and Wealth review.

e. Compete with Private Wealth Management outfits in sophistication and acquire clients from them and like them.

f. Transparent Advisory Value Add identification

g. Ability to automatically charge and collect fees automatically

h. Access to institutionalised process of Tactical Asset Allocation & Fund Manager selection. Citadelle's independent coverage of 2000+ companies & Funds, to impartially evaluate the investment choices of the fund managers.

Benefits to clients

a. Transparency in Advisory Value Add

b. Ease of execution and required reporting

c. Ability to get the best from an advisor irrespective of size

d. Confidence in the IFA who is backed by a robust process

WF: Many IFAs may have reservations about offering a PMS for mutual funds as it would seem to be an outsourcing of their key activity - which is fund selection and asset allocation. How do you propose to deal with these reservations?

Srikanth: While on the face of it, it may appear so, I think in reality what they may be actually out-sourcing is Tactical Asset Allocation (asset class and sub-asset class timing) much more than the Fund selection. Let me elaborate. ..

The process to arrive at the fund selection for different risk profiles, an advisor typically embarks upon a quantitative and qualitative assessment (Fund manager interactions etc.) of a fund. This, would then be matched with their own tactical markets views to find out which fund is likely to do best under a given market condition. An advisor then applies his assessment as a combination of the funds in the context of risk profiles and market situation. If this combination of process of qualitative, quantitative assessment along with application of these funds in the context of risk profiles is followed, the deviation in fund selection generally would not be wide. Our examination of many portfolios across organisations and individuals only confirm the same.

Now to undertake this robust process, an IFA he needs to devote time, build access to the fund manager and analysts, and have an independent ability to assess their views to finally form their own. All this can be exhausting and time consuming to do so regularly.

If therefore funds are similar, what then causes sizeable difference in client's performances of the same advisor. The difference is largely attributable to the timing of the selection and the proportion between funds for each customer. The deviations become starker due to executional challenges of reaching out to several clients in the shortest possible time, whenever ones needs to rebalance, change his fund selection. Which is where we offer our services with an acknowledgement that there will be deviations between their selection and ours. But as our back testing proves, tactical asset allocation process adds more value to clients that is attributable to advisors, than that may accrue by Fund Manager selection.

We hope advisors can see this as an aspect of communication to the client, which we believe can be made by highlighting overall benefits in the efficient arrangement that comes with no additional overall cost (including opportunity & efficiency costs) to either them or their clients

WF: Do you see this proposition gaining traction if MFDs are finally told not to offer any kind of basic or incidental advice - as is being proposed in SEBI's discussion draft on RIA regulations?

Srikanth: Absolutely! Once the RIA regulation is implemented, all an MFD may be allowed to do, is explain the features of a product and let the client decide whether to invest or no. He may even be required to prove that this is all he has done. This will result in weakening of the Client-Advisor relationship as there would be no visible value add from an MFD. In such a likely scenario, this product would enable an MFD to offer Wealth Advisory proposition until he makes up his mind about being an RIA. This would also help them with continuity of their business models and business plans without affecting their future with their clients due to regulations.

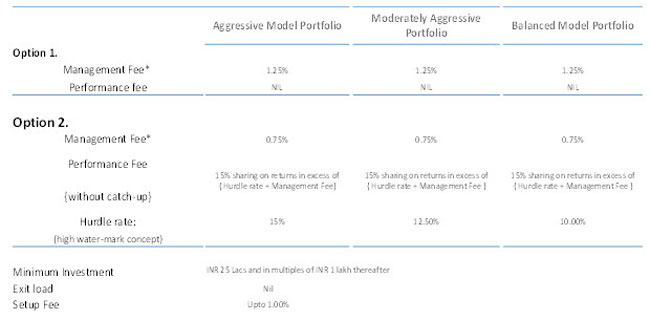

WF: What are the cost structures and the fee models in this proposition?

Srikanth: The cost structure has been designed such that there is no additional overall burden to clients or advisors. Direct plans of all selected funds will be purchased in this arrangement. We have two options to suit the client and advisor preferences that offer a flexibility to keep it within a range

WF: Do you see IFAs using this primarily as a client acquisition vehicle or as an outsourcing strategy for clients they don't have the bandwidth to personally manage?

Srikanth: Yes ! Both of them are true. The other benefits include the ability to go after scale without diluting quality to any client, savings of time and overall costs of growing his business.

Share this article

|

Advisor Speak

Advisor Speak