|

It is a strange world that we live in. Investors in times past used to get interest for the amounts they put in financial instruments. Today the chances are that not only will you get nothing, you may even be paying for the pleasure of making a deposit! Welcome to the world of Zero Interest Rate Policy (ZIRP) and Negative Interest Rate Policy (NIRP).

The Background

Arguably, the Financial Crisis of 2008 was caused (as shown so presciently by Raghuram Rajan) by interest rates held artificially low by central banks as well as by lavishly available credit. In the aftermath of the crisis, central banks in the advanced economies scrambled to further cut rates, while introducing more money into the system in the form of Quantitative Easing (QE). This meant that central banks were willing to print more money, while charging next to nothing for the use of that money. This was done out of fear that otherwise the world economy could slip into another thirties style Great Depression.

Zero interest bonds

Central banks have always played a major role in the markets. They manipulate the short term interest rates, which in turn influence the long term market set interest rates. But the current mania for low or even zero interest rates and extensive bond purchases by central banks have distorted markets and have thrown the bond markets into turmoil.

A zero interest rate bond works in this way. It is sold at a deep discount, often up to 30% of the face value. The buyer instead of earning a steady interest over a certain period has now to wait for maturity of the bond, or for another buyer who pays more than the initial offer price, to realise his/her investment.

In its present avatar the problem is that zero coupon bonds are being offered at a premium to the face value! Thus a 'buy and hold' investor would be bound to lose money. This forces the investor to attract someone who is prepared to pay an even higher amount in order to recoup his/her investment. The implication is that the new buyer may incur a bigger loss if he/she is unable to off load the bonds at a yet higher price.

Today's low interest rate ecosystem

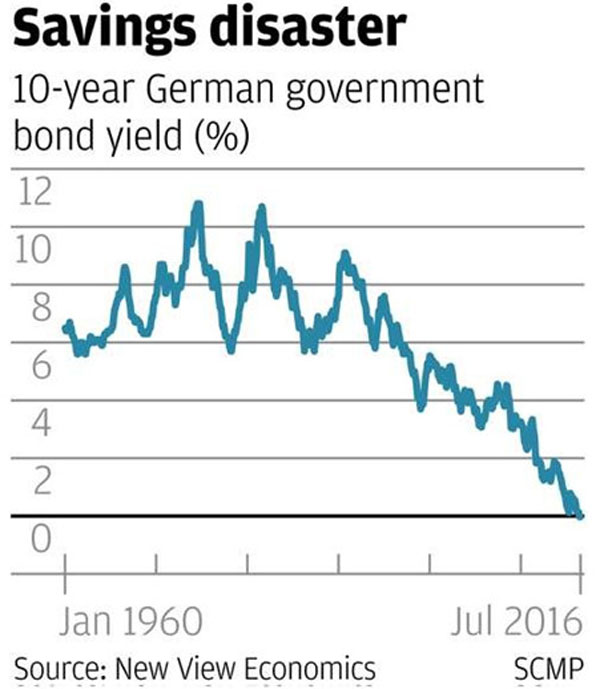

The Bank of England's 30 year yield bond which was at 2.3% a few months ago now earns just 1.3%. In Germany bonds have declined the most, pulled by the European Central Bank's, ECB, bond purchases and zero interest rates. German two year notes no longer pay any interest. Germany now has more than 160 billion euros worth of zero interest bonds. Surprisingly, Germany, in July, issued 10 year zero interest bonds at an above par price.

Gary Christenson quotes John Rubino in 'TheDeviantInvestor', "Yesterday Japan's government borrowed money on terms that require the lenders to pay rather than receive interest for ten years. And not only was that bond issue snapped up, it was vastly oversubscribed. This raises a lot of questions, the chief being 'why would anyone voluntarily commit to something that's guaranteed to lose money for a decade?'

The short, obvious answer is that the world's central banks are creating so much excess cash that there seems to be nowhere else for it to go." (March 14th, 2016)

About low interest rates

The founder of the Austrian school of economics, Ludwig Von Mises, wrote in 1909 that "…a falling value of money goes hand in hand with a rising rate of interest and a rising value of money with a falling rate of interest. This lasts as long as the movement of the objective exchange-value continues. When this ceases, then the rate of interest is re-established at the level dictated by the general economic situation." (GoldMoney Alasdair Macleod August 14, 2015)

Historically interest rates have proved stable. If prices rise, naturally businessmen would jump at the opportunity of making more profits and hence would be willing to pay higher interest rates to generate the funds to take advantage of the opportunities. In theory, lower interest rates then would prompt businessmen to borrow more. In reality it may not work that way. For investments to be profitable, the marginal gains of the extra borrowings must exceed the costs of production. A normal business with a sound balance sheet would first increase investments by using its own resources. Outside funds would be sought only if there is a significant upgrade of existing products and services, introduction of new products and services, or a major expansion of capacities. All this implies risk. Around the world, it is this willingness to take risks that is missing in today's economic scenario.

Savings and Savers damaged

The policy of the central banks has degraded the system by which peoples' savings are converted into capital for productive uses by entrepreneurs. From putting hard earned money in bank deposits, bonds and other savings instruments to earn steady and safe interest, savers are now forced to look to risky stock markets for returns by way of capital gains. Thus the monetary incentive to save is dampened, while savers may increase current consumption; a main objective of central banks' policies. Curiously enough the opposite too seems likely. Savers would realise that in order to have a defined sum as corpus on retirement day, they would have to save more and more as interest rates fall. Thus a lowering of interest rates would lead to even greater savings despite the fact that people earn less on those assets. Thus savers are battered on both sides, as it were; first because there are few sound interest bearing instruments and again because they would have to save more and curtail current consumption to reach the desired savings targets. In this scenario, the policy of low interest rates defeats its own objective of increasing consumption.

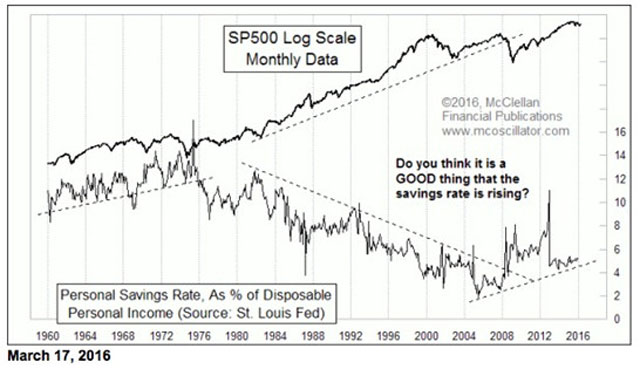

Stockcharts.com

Continuing Folly and Asset Prices

Even if there was some justification for the above policies earlier, there is no logic in continuing the same policy now, eight years after the Crisis. Advanced economies show no signs of more than tepid performances, which are passed off as 'recovery' by the powers that be. The only visible results have been an increase in government debt and an increase in asset prices, particularly stock prices.

Housing prices have risen to pre-crisis highs in most countries, while stock prices are above historical valuations. No doubt higher asset prices have helped reduce leverage, yet the debt burden is still high compared to historical averages. Most people are reluctant to spend. Wages and salaries are moving up and energy prices are cheap. A reason could be that the increase in asset prices benefitted the high net worth group most. These people, who tend to save the most, now have fewer opportunities for profitable investments. In the face of slack demand, corporations have preferred to return money to shareholders in the form of buybacks, rather than undertake risky but potentially profitable new ventures.

Normalising interest rates

The liquidity injected into the global financial system via several stimulus measures by all the main central banks, from the US Federal Reserve, through the European Central Bank to the Bank of Japan has kept interest rates low for years. Moreover with every fresh stimulus, it becomes increasingly difficult, if not entirely impossible to bring interest rates back to 'normal'.

Bringing interest rates back to 'normal' might risk a stock market collapse. Such an event would set off a rash of bankruptcies by companies still burdened with debt. This would lead to another financial crisis and possibly a depression. As Alasdair Macleod writes in GoldMoney, "After all, with the Fed funds rate at 0.25% and $2.6 trillion of commercial bank funds already on deposit at the Fed, could it be that even a small increase in the rate will just suck more deposit money out of the US banking system, leading to a contraction of bank lending?" (Lewrockwell.com, August 14, 2015)

Further, Japan has tried similar policies in the last couple of decades, without any tangible improvement to its economy. Japan is living proof that such policies are infructuous.

Any increase in interest rates is likely to increase commodity prices. Investors and speculators would find commodities more attractive than financial assets for investing.

Buying bonds, no longer safe

In this scenario it would not be out of place to say that these bonds are no longer the safe and secure instruments of yore. Too, bonds no longer pay interest, their most attractive feature, for cautious investors. Instead, they have turned into a financial device whereby speculative investors gamble that prices would continually increase. Since investors will have to wait for a long time to realise their investments, even small movements in yields would have a major impact on bond prices. It can be easily seen that these instruments would be very volatile.

Bonds were looked at as a 'safe' investment, bringing in a regular income. In the topsy-turvy world of zero interest bonds, they have become an instrument for speculation and major risk.

Share your thoughts and perspectives

Do you have any observations or insights or perspectives to share on this issue? Did this help you understand the topic better? Do you disagree with some of the observations? Please post your comments in the box below ..... it's YOUR forum !

Share this article

|