|

WF: What is the new multi-scheme SIP facility that you have launched and how does it benefit investors and distributors?

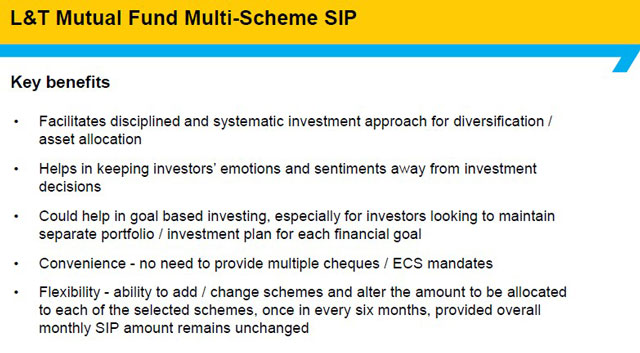

Kailash: We all know that a SIP is a healthy investing habit and retail investors should look at investing systematically in these volatile times. Major distribution partners across the length and breadth the country raised an issue in connection with SIPs, which is in terms of administrative work because for every SIP they have to fill up a separate form and a separate debit mandate. They find it very cumbersome. At the same time, they are keen to offer an appropriate asset allocation within the SIPs they recommend. Now, the only way in which they can offer asset allocation and reduce paperwork is to go for asset allocation products, which may not be ideal for many investors and distributors, as most have pre-defined allocations.

Our objective of coming up with Multi-Scheme SIP was to take away the administrative hurdles that distributors face, yet give them and their clients flexibility in asset allocation. In our Multi-Scheme SIP, you can participate in three of our schemes at one time by filling up just one form, giving one cheque and only one debit mandate. It clearly reduces the administrative work that distributors have to do. There is no fixed asset allocation as well. We have left it to the choice of the investor on how he wants to allocate the money because we believe that different investors have different risk profiles and different wants and we cannot dictate the choice. Investors can choose equity and debt schemes from our fund range or can choose three different equity schemes, or a combination of equity, hybrids and debt - as per their risk profile.

We have also added a feature where you can add or change schemes or change the amounts allocated to each of the 3 schemes once in 6 months, so long as the overall SIP amount remains unchanged. If the advisor and client believe during a review, that they may wish to enhance allocation to one asset class and reduce another, there is no need for going through fresh documentation - you can continue with the Multi-Scheme SIP and simply alter the allocation. This makes execution of portfolio review decisions also very convenient for the investor and the advisor.

WF: One angle of this new facility that you are particularly excited about is its ability to help distributors increase their wallet share significantly from existing clients. How do you see this happening?

Kailash: Whenever we have conversations with distributors, the common issues most have is about how to increase AuM, how to increase wallet share from existing clients, how to acquire new clients. I think our Multi-Scheme SIP is a great tool for distributors to enhance their AuM.

Our industry has been talking about liquid funds as an attractive alternative to idle savings account balances for some time now. However, many distributors have so far been a little reluctant to make an all-out effort in this direction as the commissions on low expense products like liquid funds is obviously much lower than on full fee products like equity and hybrid funds. Many distributors would rather make more efforts on getting the incremental equity or hybrid SIP than on focusing on liquid SIPs as an alternative to savings account balances.

What we are now saying to all distributors is that with Multi-Scheme SIP, you can now do both - go after equity and hybrid SIPs as well as liquid SIPs - within the same effort. A typical investor who saves say Rs.10,000 per month, will perhaps be comfortable with SIPs to the tune of Rs. 4000 - 5000, but rarely will he put away all 10,000 in SIPs and have nothing available as liquidity. Now, with Multi-Scheme SIP, the distributor can go for that 4000 rupees that may go into equity or hybrid SIPs and at the same time, with no incremental effort, advise the client to park the balance 5000 to 6000 rupees in our liquid fund. Returns are obviously superior to a 4% taxable interest on savings accounts - but customers will obviously want comfort on the safety and liquidity aspects as well. Once a distributor demonstrates this, he should be able to get his clients to not only invest with him but also save with him. Getting clients to save with you is absolutely critical for you to have a say in where these accumulated savings finally get invested. It is quite possible that 8 to 10 months later, you can go back to the client and show him how his savings in liquid SIPs have steadily grown and enquire about what the client plans to do with these accumulated savings. That can in turn open up avenues for you to suggest funds in accordance with your client's risk profile.

What we are saying is simple : if you believed that getting clients to only save with you is not very remunerative, please use our Multi-Scheme SIP to get clients to invest and save with you. This makes the whole proposition win-win for you and your client. I believe if distributors put a focused effort in this manner, they can significantly enhance their AuM from existing clients as well as pitch for larger allocations from new clients.

We need to keep in mind that most of your clients either have a significant build up of idle balances in their savings accounts over several months or are actively maintaining recurring deposits with banks. We all know that SIPs in liquid funds offers a superior alternative to both. If the hitch so far was an effort - reward correlation for the distributor, we are now addressing this issue with Multi-Scheme SIPs.

Also, at a time when investors are saving more and investing less due to market volatility, why only pitch for SIPs from a diminished investment allocation? Why not pitch for the entire amount - whether it goes into savings or investment avenues?

If we just do the math, if a distributor is able to target 100 of his existing customers and get Rs.10000 per month into Multi-Scheme SIPs - in any combination of liquid, hybrid, debt and equity schemes, we are effectively talking of enhancing his AUM by Rs.10 lakhs per month or Rs. 1.2 crores per annum, which is not a small amount especially in these times when customers are not willing to give you money and want to keep it in their savings accounts for higher safety. Once you have got your client to commit to a 10,000 rupees per month savings and investment plan with you, you can always jointly decide every six months whether you wish to alter the allocation between liquid and equity SIPs, without impacting the overall plan. This way, you may find it a lot easier to get clients to commit to larger SIPs with you.

Share this article

|

On the face of it, L&T MF's new Multi-Scheme SIP looks like a good convenience enhancer - fill one form instead of three. But that's just one of its benefits, says Kailash as he explains how distributors can not only provide convenience to their clients, but can actually use this new facility as a growth driver for themselves. Read on as Kailash explains how you can intelligently use this new facility from L&T MF to grow your AuM, apart from enhancing convenience for your clients.

On the face of it, L&T MF's new Multi-Scheme SIP looks like a good convenience enhancer - fill one form instead of three. But that's just one of its benefits, says Kailash as he explains how distributors can not only provide convenience to their clients, but can actually use this new facility as a growth driver for themselves. Read on as Kailash explains how you can intelligently use this new facility from L&T MF to grow your AuM, apart from enhancing convenience for your clients.