Listen to a summary of Michael Hasenstab's views on emerging markets in this brief video:

Michael Hasenstab, Ph.D.

Executive Vice President, Portfolio Manager

Chief Investment Officer

Templeton Global Macro

The last several years have been trying for emerging markets, with 2015 marking the fifth consecutive year of decelerating growth. As the immediate recovery post-global financial crisis (GFC) was exceptionally strong, some deceleration was always in the cards. Over the last few years, however, the normal cyclical slowdown has been aggravated by severe and interlinked shocks. However, despite the severity of the shocks, they have not triggered another systemic emerging market (EM) crisis along the lines of those seen in the 1990s. Instead, these shocks have so far resulted mostly in slower economic growth, rather than the severe crisis that appears to be priced in. We believe the reason for this surprising resilience lies in the lessons that EMs have learned from previous financial crises, and which allowed many, albeit not all, of them to build substantial buffers and safeguards.

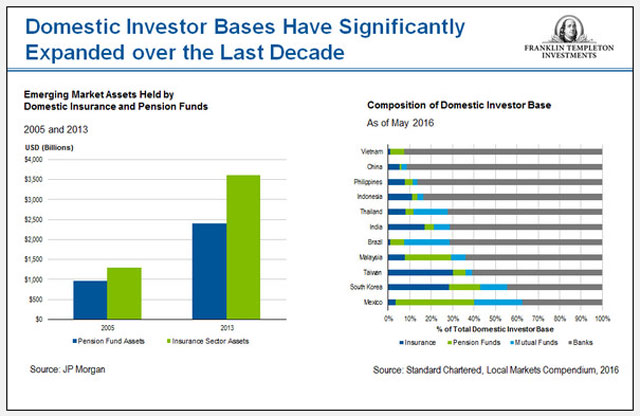

Perhaps the most important step that emerging markets have taken to reduce their vulnerability to financial crises is the remarkable deepening of domestic financial markets over the past decade. In many countries, the development of a reliable domestic investor base has benefited from the rise of a broad middle class. For example, the total assets held by domestic insurers and pension funds in emerging markets have swelled from US$2.3 trillion in 2005 to around US$6 trillion in 2013, boosted by the expansion of the insurance sector in EM Asia and by pension funds in Latin America.1 Mexico stands out in its reduced reliance on the banking sector as a source of domestic funds. This transition toward more balanced funding has improved financial resilience. Domestic institutional investors can be a stabilizing force when asset prices collapse to levels that are clearly out of line with fundamentals-in the past, the lack of a strong domestic investor base often magnified the consequences of financial volatility.

Of course, financial risks also vary considerably across regions and countries. However, a few common themes do seem to hold. First, contagion risk seems to have diminished. The same transmission mechanisms through financial linkages, trade and competitive currency devaluations have been operating in the past several years, but they have not overwhelmed economies in such a violent manner as in past episodes. Second, most recent crises have been relatively contained currency crises, as in the case of Brazil, without immediately cascading to the banking system. Overall, the lines of defense have widened; policymakers in many countries have more options and time to react when volatility picks up and their economies come under pressure. Although debt levels have increased in emerging markets since the GFC, these developments point to some degree of improvement in the robustness of the financial architecture in many countries and suggest a greater level of resilience at the global level than in the past.

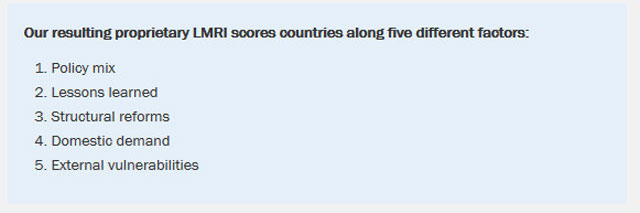

Recognizing the major changes that EMs have experienced over the past decade, we have laid out a new framework to assess the investment risks and opportunities in individual markets. Our framework extends beyond the traditional indicators of external vulnerability, recognizing the much greater importance of local debt markets. Our framework therefore focuses on the strength of domestic demand, the quality of macroeconomic policies, and the extent to which individual countries have learned the lessons of past crises. Based on this framework we developed our proprietary Local Markets Resilience Index (LMRI) to rank countries in terms of both their current and projected conditions. We believe this methodology provides a much better roadmap to investment opportunities than the narrow focus on external vulnerabilities that still prevails in financial markets.

For each factor, we separately assess both current and projected conditions, so as to gauge the degree of risk along the investment horizon. We aggregate the five individual category scores to obtain an overall country score-our proprietary LMRI. The scoring along each category is necessarily based to an important extent on our subjective judgment; nonetheless, we believe it provides a strong rigor in assessing and comparing different markets in a way that allows us to assess the true underlying risk and to identify attractive opportunities where our score deviates significantly from the risk assessment implicit in market prices.

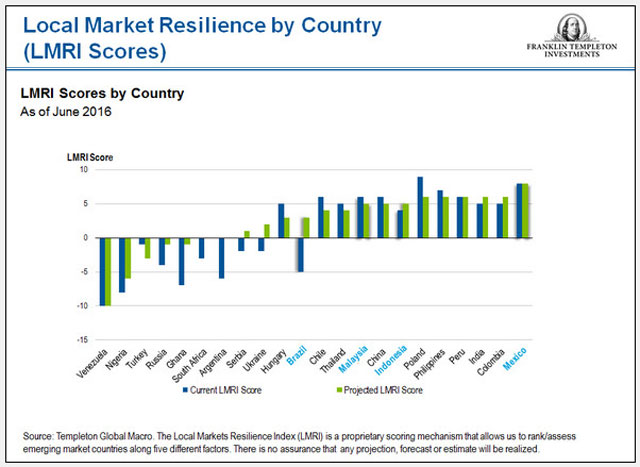

The rating of countries is based on the five criteria, described above. Each criterion is assigned a value between -2 and +2 for the current situation, and similarly a value for the projected outlook, in the views of the team. The chart below shows the results of our ranking system for the selected subset of EMs across the different regions.

Our case studies illustrate some aspects of the research the group undertakes in analyzing individual countries, together with the scoring for each. We have picked Mexico, Brazil, Indonesia and Malaysia.

Summary of our LMRI Rating for Mexico

Mexico is the textbook case of a country that has taken to heart the lessons of previous crises and moved to not only reduce macroeconomic vulnerabilities, but also launch wide-ranging structural reforms. In our LMRI, Mexico earns the highest scores for Lessons Learned-Mexico adopted a flexible exchange rate, built up foreign exchange reserves and reduced short-term debt-and Structural Reforms, both current and forward-looking, where the depth and breadth of Mexico's recent efforts stand out among emerging markets; the Policy Mix is strong and getting stronger, with prudent fiscal policy that has reduced dependence on oil revenues, and a proactive monetary policy; External Vulnerability is limited, as the share of oil in total exports has been steadily declining in favor of manufactured products; and Domestic Demand is very strong, thanks to healthy real wage growth and low unemployment, though we expect some weakening ahead due to the ongoing fiscal consolidation. Overall, Mexico scores close to the maximum on our LMRI, both current and forward-looking.

Summary of our LMRI Rating for Brazil

Brazil stands out as a vulnerable market that is, however, poised for a significant rebound, in our assessment. In our LMRI, Brazil earns a decent score for Lessons Learned: Brazil adopted a flexible exchange rate, has strong foreign exchange (FX) reserves and limited short-term debt; this is also reflected in a moderate and improving External Vulnerability score, with its reliance on commodities being the Achilles heel. Current scores for Policy Mix, Structural Reforms and Domestic Demand are at the lowest levels, as reflected in the combination of deep recession and political turmoil. However, we project a stabilization in Domestic Demand, a marked improvement in Policy Mix (in some areas already underway) with a new administration in place, and some improvement in Structural Reforms.

Summary of our LMRI Rating for Indonesia

Indonesia is a consistently good performer across most of our key factors. In our LMRI, Indonesia earns the top score for Domestic Demand, both current and forward-looking, underpinned by favorable demographics; a strong score for Policy Mix, current and future, thanks to prudent fiscal policy and recent subsidy reforms; a moderate and stable External Vulnerability score, supported by a healthy level of FX reserves; a Structural Reforms score in the middle of the range, with some improvement projected in the future-Indonesia needs more investment in infrastructure; and a Lessons Learned score at a strong +1 both current and forward-looking-the country has taken to heart the lessons of the Asian financial crisis, adopting a flexible exchange rate and maintaining healthy levels of FX reserves.

Summary of our LMRI Rating for Malaysia

Malaysia is a very good performer based on our metrics. Our LMRI highlights Malaysia's very strong Domestic Demand, though with some weakening projected ahead; Malaysia earns top scores for Lessons Learned, both current and forward-looking, reflecting its adoption of a flexible exchange rate and prudent macro policies; it scores well on Structural Reforms, thanks to strong institutions and transparency, though we see headwinds ahead for further reform implementation; Policy Mix scores at a strong +1 both current and forward-looking, in recognition of the ongoing fiscal consolidation and prudent monetary policy; and External Vulnerability is limited, thanks to the high degree of export diversification, and is projected to improve further.

Global Environment

United States

The US economic recovery remains steady, dispelling market fears earlier this year of impending recession. First-quarter (Q1) 2016 gross domestic product (GDP) growth was relatively low, at 0.8%, but this mostly reflects well-known seasonality issues.2 In a recent speech, San Francisco Federal Reserve (Fed) President John Williams noted that according to his staff's analysis adjusting for residual seasonality in Q1 indicated true real GDP growth above 2%.3 Furthermore, over the last few months, activity indicators have been strong across the board: Consumer confidence is running near record-high levels, retail sales are strong and the housing market remains resilient.

The labor market has strengthened further: Job creation continues to outpace the increase in the labor force, and the unemployment rate has dropped to 4.7% in conjunction with some recovery in the participation rate. The only notable exception was the May payroll figure, which was unexpectedly low: While the pace of job creation should naturally slow as we are at or close to full employment, the 38,000 nonfarm payroll (NFP) figure appears to be an outlier, inconsistent with all other labor market indicators that show continued strength. The tighter labor market conditions have recently begun to translate into more robust wage pressures: The Atlanta Fed composite wage indicator accelerated to 3.4% year-over-year (yoy) in April, the strongest growth since early 2009.4

As we had foreshadowed in our previous edition of Global Macro Shifts (GMS 4),5 headline inflation has started to rise. Core inflation has remained stable at around 2%, suggesting that the previous decline in headline inflation reflected lower energy prices, and not weaker economic activity or broader disinflationary trends. Since early this year, oil prices have first stabilized, and then recovered to a somewhat stronger degree than was anticipated. In GMS 4, we designed a model to forecast inflation. We noted that even if oil prices remained at the US$30 per barrel (pb) levels that were prevalent at the start of the year for the remainder of 2016, the adverse base effect impact on headline inflation would likely fade out by January 2017. This would then set the stage for a rebound in consumer prices.6 Since then, oil prices have, in fact, rebounded to about US$50 pb rather than remaining at US$30, suggesting that the recovery in headline inflation is likely to continue in the months ahead and at a faster pace.

In other words, recent data on activity, wages and inflation have vindicated the out-of-consensus view that we articulated at the beginning of the year in our GMS: namely that inflation was set to rebound, with risks tilted to the upside.

These developments on activity and inflation were reflected in somewhat more hawkish Fed rhetoric during April and May, when a series of public statements by Fed officials indicated that a second increase in policy interest rates might be appropriate already at the June Federal Open Market Committee (FOMC) meeting-a view repeated in the April FOMC minutes. This forced financial markets to rapidly revise upward the probability of an interest-rate hike in either June or July, previously priced out. The May NFP number, however, has pushed the Fed back to a more cautious stance: The bank kept rates on hold at the June meeting, and the "dots" shifted lower, signaling that FOMC members on average now expect a less aggressive tightening cycle this year. This shift in Fed stance was once again quickly reflected in market expectations.

The frequent swings in the Fed's rhetoric have undermined the bank's credibility, especially in light of generally robust economic developments. Following the December 2015 rate hike, the Fed had indicated that an additional four hikes would probably be appropriate over the course of 2016. Following another round of declines in oil prices and equity prices at the beginning of the year, the Fed adopted a more dovish tone, stressing downside risks to global growth, and leading the market to expect little or no change in policy interest rates for the year. During the hawkish shift in tone in April-May, financial markets' rate expectations lagged behind the indication of the Fed's "dots," suggesting that they expected the Fed might once again change its stance-which indeed happened in June.

We continue to believe that trends in US growth and inflation will require a further significant tightening of monetary policy. In fact, recent developments underscore, in our view, the rising risk that the Fed might fall behind the curve with its monetary policy response. If that were the case, during the course of 2017 the Fed might find itself forced to raise interest rates faster than it is currently envisaging, and much faster than markets currently anticipate.

Japan

Meanwhile, the Bank of Japan (BOJ) followed in the path of the European Central Bank (ECB), Sweden's Riksbank and the Swiss National Bank into the territory of negative interest rates. The BOJ took its monetary policy rate to -10 basis points (bps) in January this year, easing by 10 bps, as it sought to counter the deflationary impact of lower energy prices. The BOJ's efforts, however, were undercut by the simultaneous shift in Fed rhetoric. In its December meeting, the Fed had led markets to believe it would hike four times during 2016. By March this had been reduced to two hikes. The market pricing of Fed rate hikes correspondingly went from about 90 bps for the year to a low of about 20 bps in February, effectively a front-end easing of 70 bps relative to December.7 In other words, the Fed's shift in rhetoric de facto more than reversed the impact of its December hike, with an effective easing that overwhelmed the BOJ's move. This resulted, unsurprisingly, in a significant appreciation of the Japanese yen versus the US dollar-even after the most recent hawkish Fed statements, the yen was about 13% stronger year-to-date through the analysis date of this paper in mid-June. The Bank of Japan has been on hold since January-in our view, the BOJ has decided that further monetary easing on its part would be ineffective until the Fed hiking cycle resumes. Looking forward, we believe that Japan's growth and inflation outlook will continue to impart an easing bias to the BOJ's policy; the eventual resumption in Fed monetary policy tightening should therefore result in a meaningful resumption of yen depreciation.

Eurozone

The ECB has also taken the road of negative interest rates, as it struggles to bring inflation and inflation expectations back to target. Eurozone growth has been relatively solid, reflecting a cyclical upswing supported by a weaker euro and accommodative monetary policy. Accumulated slack in the economy, however, has kept price pressures muted, and we expect that ECB monetary policy will remain loose for a while and lag the Fed's tightening cycle.

China

Our view on China has not changed. Policymakers have stepped in to prevent a further deceleration in GDP growth, through higher credit growth and some recovery in infrastructure investment. Most recent activity data suggest that the moves have been generally successful, and we continue to believe that China will sustain a soft landing into 2017, striking a delicate balance between supporting growth and maintaining sufficient reform momentum. China's outlook remains characterized by the classic policy "trilemma," namely the impossibility of reconciling a flexible exchange rate, capital flows liberalization and independent monetary policy. Earlier this year, financial markets feared that China would square the circle through a substantial exchange rate depreciation aimed at boosting growth. We believed that China would instead square the circle by slowing, and in some cases reversing, the process of capital account liberalization. Capital controls could be used to stem the loss in FX reserves and take the immediate pressure off the exchange rate, while allowing a gradual depreciation. China's government has indeed moved along these lines, and we expect this strategy to continue.

For a more detailed analysis, read "Emerging Markets: Mapping the Opportunities" a research-based briefing on global economies featuring the analysis and views of Dr. Michael Hasenstab and senior members of Templeton Global Macro. Dr. Hasenstab and his team manage Templeton's global bond strategies, including unconstrained fixed income, currency and global macro. This economic team, trained in some of the leading universities in the world, integrates global macroeconomic analysis with in-depth country research to help identify long-term imbalances that translate to investment opportunities.

The comments, opinions and analyses are the personal views expressed by the investment manager and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice, and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton Investments ("FTI") has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

Get more perspectives from Franklin Templeton Investments delivered to your inbox. Subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_Global and on LinkedIn.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets' smaller size and lesser liquidity.

1. Source: JP Morgan.

2.. Source: Bureau of Economic Analysis. This figure is quarter-over-quarter, seasonally adjusted at an annualized rate (qoq, saar).

3. Source: Federal Reserve Bank of San Francisco.

4. Source: The Atlanta Fed wage index tracks the median wage growth for a matched sample of workers (workers employed continuously at same place for 12 months) to control for composition effects.

5. Source: Inflation: Dead, or Just Forgotten? (GMS 4) Templeton Global Macro, Franklin Templeton Investments, February 2016.

6. In GMS 4, we tested seven different alternative specifications of a Phillips curve relationship. We chose the best forecasting model by minimizing the root mean square error of the forecasts compared to the realized values of inflation. Using our preferred specification to forecast the four-quarters-ahead inflation rate we projected that, based on fundamentals at the time, headline inflation would be greater than 2% by end 2016. We then incorporated into the model, the impact of oil price decline over the course of 2015, and showed the impact of oil prices not recovering from the US$30/barrel level.

7. Source: Calculations by Templeton Global Macro using data sourced from Bloomberg. Rates expectations calculated using one-year forwards versus three-month LIBOR as a proxy.

Share this article

|

Equity Insights Global Perspectives

Equity Insights Global Perspectives