|

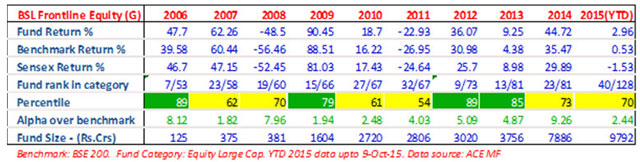

Click here to know more about percentiles and the colour codes

What do percentiles and their colours signify?

Fund performance is typically measured against benchmark (alpha) and against competition.

Performance versus competition is measured through percentile scores - ie, what

percentage of funds in the same category did this fund beat in the particular period?

If a fund's rank in a year was 6/25 it means that it stood 6th among a total of

25 funds in that category, in that period. This means 5 funds did better than this

fund. In percentile terms, it stood at the 80th percentile - which means 20% of

funds did better than this fund, in that particular period. If, in the next year,

its rank was 11/26, it means 10 other funds out of a universe of 26 did better than

this fund - or 38% of funds did better than this one. Its percentile score is therefore

62% - which signifies it beat 62% of competition.

Most fund managers aim to be in the top quartile (75 percentile or higher) while

second quartile is also an acceptable outcome (beating 50 to 75% of competition).

What is generally not acceptable is to be in the 3rd or 4th quartiles (beating less

than 50% of competition). Accordingly, we have given colour codes aligned with how

fund houses see their own percentile scores. Green colour signifies top quartile

(percentile score of 75 and above), yellow or amber signifies second quartile (percentile

scores of 50 to 74) and red signifies 3rd and 4th quartile performance. A simple

visual inspection of colour codes can thus give you an idea of how often this fund

has been in the top half of the table and how often it slips to the bottom half.

A great fund performance is one which has only greens and yellows and no reds -

admittedly a tall ask!

WF: BSL Frontline has charted a fantastic 10 year journey, rising from a 7 cr fund to one that's now close to 10,000 crores, and an acknowledged leader in the large cap funds space. Looking back, what would you say is the single biggest driver of the phenomenal success of this fund, in one of the most competitive categories within the equity funds space?

Mahesh Patil: Yes, the fund has indeed grown very well over the last 10 years that I have been managing it. In these 10 years, we have seen different phases of the market - the very bullish phase from 2005 to 2007, then the global financial crisis of 2008, then a short and sharp recovery, then a prolonged sideways phase and now the recent upmove. Through each phase, there were a lot of learnings, and our constant endeavor was to learn and evolve as we went along.

Our focus from the beginning was to look at each year, and target to beat the benchmark, each year. Keeping that focus on beating benchmark Y-o-Y helped bring in a lot of discipline and focus. I would say the key success drivers for us have been:

Discipline: We always kept our objective in mind, of trying to beat benchmark y-o-y. This guided us to take measured risks at all points in time Balanced: We tried to avoid going overboard in any direction, or in any sector, or following any trend. We kept reminding ourselves that mean reversion always happens, and that kept us from getting carried away. Stock picking: Discipline and balance in approach help only if the main engine - stock picking - is doing well. That's been a big contributor to our success. We have a great research team that keeps identifying good ideas. We maintain a healthy balance between generating new ideas and maintaining focus on existing ideas. Adaptability: Finally, as markets go through different phases of a cycle, you need to adapt your strategy to suit market conditions. You need to maintain consistency of philosophy, but retain a nimbleness to respond to changing market conditions. This is especially important when you set yourself a target of trying to achieve alpha on a Y-o-Y basis. Being nimble and adapting our strategy to market phases has I think been a significant contributor to our success.

WF: It is often said that success comes not from only doing the right things, but equally from avoiding pitfalls. Looking back, what were some of the biggest temptations you resisted, which later proved to be pitfalls that perhaps impacted several others?

Mahesh Patil: Each phase of the market teaches us a lot. We make mistakes. But the key is to learn and imbibe, so that you keep refining your portfolio strategy, based on each new learning. Take the financial crisis of 2008. That crisis taught us that if you positioned your fund in a particular direction and there are large shocks in the market; what counts is your ability to take corrective action post the shock. Your stock and sector exposures, the liquidity of stocks you own - all of these are important considerations when you try to realign your portfolio after a shock. The global financial crisis taught us some valuable lessons, which we have imbibed in our portfolio strategy.

Then there was the Satyam shock - it fell more than 50% on that one fateful day. We had a 2% exposure in our fund to Satyam. That episode taught us more insights into evaluating management quality, some of which are not very obvious.

A third big learning for us is pay equal attention to the portion of the portfolio that is underperforming as we would normally like to do with the portion that is outperforming. Often, we as portfolio managers get wedded to stocks that are underperforming - we find it difficult to accept the market's verdict on the stock and keep hoping for market to align with our own thinking. This drags down overall portfolio performance. One has to learn to be more objective and less emotional when looking at each stock in the portfolio and its contribution towards generating overall portfolio alpha. One has to learn to take hard decisions in the interest of overall portfolio performance.

So, I think what has helped us is not that we didn't make mistakes, but that we learned from them and incorporated these learnings in constantly fine-tuning our portfolio strategy.

WF: It seems that what has enabled you to have this unblemished record over the last 10 years of Y-o-Y alpha and Y-o-Y 1st / 2nd quartile performance is a sort of "goldilocks" equation or fine balance between good stock picking, stringent discipline and constant learning and fine tuning. Would that be a fair comment?

Mahesh Patil: I would say it's a mixed skill; you can't overly depend on any one of them - you got to manage all the variables in a sensible and prudent manner. Alpha ideas is also about maintaining a good balance between top down views and bottom up stock ideas. So yes, a judicious mix is what helps maintain consistency in performance.

Our goals are very clear - to try and deliver positive alpha on a year-on-year basis, and to be placed within 1st / 2nd quartile in the peer group, year-on-year. Our study of relative performance over several years indicates that if you achieve a 300-400 bps alpha each year, there is a very good chance of being placed in 1st or 2nd quartile in the peer group. So, really what we work towards is to try and achieve a 300-400 bps alpha each year. If we do that, both our objectives get achieved.

WF: Looking ahead, how do you see the near to medium term prospects for large caps?

Mahesh Patil: If you look at large caps, they have significantly underperformed mid caps in the last one and half years. Since we have not seen any major earnings delta in the last one and half years, it logically follows that midcaps have become more expensive than the large caps. Relatively if you look at it today, if you want to construct the portfolio on a risk adjusted basis, I think large caps would look the better option - from a risk adjusted basis. Large caps are by and large trading around their long term averages, barring a few outliers, while midcaps are trading a little above their long term averages.

Having said that, we must also recognize that midcaps generally do better than large caps in an economic upswing. We believe we are at the cusp of an economic upswing, therefore over the next 3 years, midcaps can perhaps deliver higher absolute returns compared to large caps.

So, it really depends on your investment objective. If you are looking at a better risk adjusted return over the medium term, large caps appear a better bet today. If you are shooting for higher absolute returns over the long term, mid caps may be a better option.

WF: Within large caps which are some of the sectors and themes that you believe hold value given that we are not yet in a very robust economic environment?

Mahesh Patil: In considering sectors and themes, we focus on outlook for stocks and sectors from a medium term (1-2 year) perspective and valuations relative to historical multiples. On this basis, the two broad themes that look attractive are businesses that benefit from Government spending and businesses that play the urban consumption theme.

We believe Government spending will continue to be the key investment driver over the next 1-2 years as compared to private sector capex. On urban consumption, we think higher real wage growth, better disposable income on the back of cutting interest rates, and some benefits coming in because of the pay commission benefits coming at least to the Government and PSU employees - all of these can help drive urban consumption.

Auto and auto ancillaries are a good play on urban consumption. Private sector banks and some NBFCs also look well poised to leverage this theme. Media sector looks good - advertising growth is strong - perhaps led by e-comm companies vying with each other to grab eyeballs. FMCG companies are also sprucing up ad budgets, which is good for the media industry.

On the government spending theme, businesses connected with roads, railways and defence look attractive. On defensives, which we would like to have an exposure to for balancing the portfolio, we continue to prefer pharma. Though valuations are a little high, many pharma companies have a good product pipeline which can sustain growth momentum. One has to however be very stock specific in pharma.

WF: What is your outlook on equity markets over the next 1-2 years? Worries continue on unstable global environment as well as continued weakness in domestic growth.

Mahesh Patil: Markets have given up gains on a year-to-date basis. Some of the froth that was built up on early recovery expectations, government push expectations etc has gone, which is healthy for the market. Valuations at a broad market level are now at long term average.

Secondly we believe that the earnings decline witnessed over the last two or three quarters, is bottoming out. I think it should bottom out with the September quarter. Going forward I think the December quarter is where you would see the base would be favorable. You will see the full benefit of the raw material prices cut, the fall in commodity prices, which will come through with a lag effect.

The benefit of the rate cuts is starting to flow in now much more visibly with the cut in the bank rates, the base rates by the banks. Probably another 50 basis points cut will come in this cycle. We have seen some signs of recovery in the economy at least on the IIP numbers which have started showing 4 to 5% growth for the past here months , after zero to negative growth for the last two years.

All these factors will start to drive economic growth. This will help the corporate sector where the top line growth has been really weak in the last few quarters. We think that in the next 12 months, there should be a trend where the base is supportive and you will see earnings growth also start to come back strongly. I would say looking at the numbers; we are expecting at least 15 to 20% earnings growth in FY17.

On the global front, we have seen a lot of that uncertainty playing out this year. We have seen huge redemptions from emerging markets funds. While there could still be some kind of volatility, I think at least from a near to medium term perspective a lot of those things have actually played out and things will normalize.

Given all these factors and valuations at reasonable levels, risk rewards look very compelling even from a medium term perspective of 12 months. I think it's time to really start building equity exposure aggressively.

Share this article

|

Fund Focus: BSL Frontline Equity Fund

Fund Focus: BSL Frontline Equity Fund