|

Click here to know more about percentiles and the colour codes

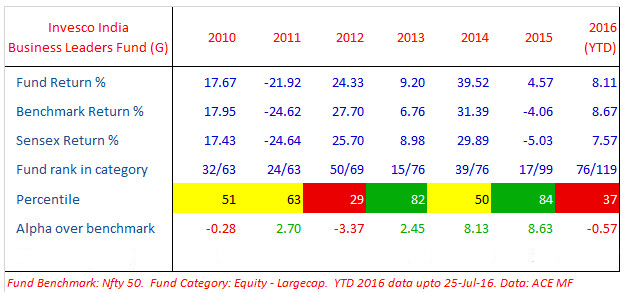

What do percentiles and their colours signify?

Fund performance is typically measured against benchmark (alpha) and against competition.

Performance versus competition is measured through percentile scores - ie, what

percentage of funds in the same category did this fund beat in the particular period?

If a fund's rank in a year was 6/25 it means that it stood 6th among a total of

25 funds in that category, in that period. This means 5 funds did better than this

fund. In percentile terms, it stood at the 80th percentile - which means 20% of

funds did better than this fund, in that particular period. If, in the next year,

its rank was 11/26, it means 10 other funds out of a universe of 26 did better than

this fund - or 38% of funds did better than this one. Its percentile score is therefore

62% - which signifies it beat 62% of competition.

Most fund managers aim to be in the top quartile (75 percentile or higher) while

second quartile is also an acceptable outcome (beating 50 to 75% of competition).

What is generally not acceptable is to be in the 3rd or 4th quartiles (beating less

than 50% of competition). Accordingly, we have given colour codes aligned with how

fund houses see their own percentile scores. Green colour signifies top quartile

(percentile score of 75 and above), yellow or amber signifies second quartile (percentile

scores of 50 to 74) and red signifies 3rd and 4th quartile performance. A simple

visual inspection of colour codes can thus give you an idea of how often this fund

has been in the top half of the table and how often it slips to the bottom half.

A great fund performance is one which has only greens and yellows and no reds -

admittedly a tall ask!

WF: Calendar year 2015 was a very good year for the fund - strong alpha and a top quartile performance. What does your attribution analysis show as the key alpha drivers?

Vetri: Our positive attribution in CY15 was due to stock selection from Consumer Discretionary and Financials Sector. Our negative attribution in the same period was due to stocks from the Telecom and Utilities sectors.

The fund has a significant growth bias and that has certainly helped performance in the recent past. In addition, having underweight positions in companies with balance sheet challenges or poor return on capital delivered positive attribution.

WF: This calendar year (YTD) has proved a little challenging. What are some of the factors impeding alpha generation and how do you propose to overcome them in the rest of the year to maintain your positive alpha YoY track record of recent years?

Vetri: Our positive attribution in YTD CY16 was due to stock selection from Energy and Financials Sector. Our negative attribution in the same period was due to stocks from the Industrials and Consumer Staples sectors.

The Fund typically invests in companies that are leaders in their sector or sub sector. We define leaders based on profitability metrics and not on revenues or market share. Our YTD performance relative to this peer group is partly because of stock picking and also because we run a very large cap biased portfolio. Only 10% of the fund is invested in companies that are outside the benchmark Index(Nifty 50).

WF: Mid and small caps are trading at a premium to large caps. Some say this means that large caps are relatively undervalued while others suggest that the premium is justified due to better earnings growth prospects in smaller companies. What is your position on this debate?

Vetri: Nifty index, representing Large Caps, currently trades at more than 20% premium to its own long period average. The premium is largely being attributed due to expectations of a superior growth in the medium term, which has failed to materialize for the last few years. Similarly, Nifty Midcap 100 index trades at a premium to the Nifty Index, compared to a discount it has traded on an average over the last 10 years. While the midcaps tend to grow faster than Large caps, especially during a cyclical macro upturn, we think the valuation risks currently outweigh potential growth tailwinds.

WF: Are the current set of earnings announcements in line with your expectations or disappointing? What trends are you seeing in terms of sectoral growth prospects from the current round of earnings?

Vetri: We are midway in the earnings seasons, and many companies have yet to report the numbers. However, from based on earnings reported till now, we are seeing a mid-single digit growth in earnings for Sensex companies.

WF: What is your stance on the PSU vs private banks debate? How is this reflected in your portfolio?

Vetri: We have been avoiding companies with poor balance sheets across sectors. The PSU banks are experiencing significant balance sheet issues due to high credit costs and their core liability franchise is also weakening. On the other hand, most private sector banks have been well run with judicious focus on both growth and capital efficiency. We do however have exposure to some private sector lenders that have experienced stress in their corporate book. However what differentiates them and gives us comfort is their current level of capital adequacy and pre provisioning profitability.

WF: How do you see the energy space shaping up in light of the Government's thinking on consolidation of PSU oil companies?

Vetri: It would be speculative to discuss the implications of a move that is yet to be announced. For now, we prefer downstream oil companies and they have higher capital efficiency and reasonable valuations.

WF: Have our markets run ahead of fundamentals? Is another round of mean reversion due? What is your sense of market direction and drivers over the next 12 months?

Vetri: The challenge for equity market is valuations. In the early part of CY 2016, the market was trading at under 10% premium to its long term average valuations on a trailing basis and was in our comfort zone. However, the rally in market post March 2016 has resulted in this PE premium expanding to more than 20%. Based on the past history of valuations, such premium valuations reduce the probability of healthy forward return outcomes. We recognize that a cyclical macro upturn can result in a stronger than average earnings growth in the medium term but the key question for us is 'how much of that is already in the valuations?'

WF: Which sectors and themes are you most overweight on in the portfolio and why?

Vetri: The biggest sector overweight is Consumer Discretionary. Valuations here, though not cheap but relative to growth prospects, they look reasonable. These companies are also enjoying a tailwind from falling interest rates are supportive of consumer demand. Our single largest weight is in Financials, but it is hard to be significantly overweight here as the sector is over 30% of the benchmark. We like Financials and like Consumer Discretionary -they should benefit from a cyclical upturn in the economy. Our biggest underweights are in Energy, where risk to commodity prices outweigh return potential and Industrials where we find valuations expensive.

DISCLAIMER: The views are expressed by Mr. Vetri Subramaniam, CIO and Mr. Vinay Paharia, Fund Manager - Invesco Asset Management (India) Private Limited. The views and opinions contained herein are for informational purposes only and should not be construed as an investment advice or recommendation to any party or solicitation to buy, sell or hold any security or to adopt any investment strategy. The views and opinions are rendered as of the date and may change without notice. The recipient should exercise due caution and/or seek appropriate professional advice before making any decision or entering into any financial obligation based on information, statement or opinion which is expressed herein. Invesco Mutual Fund/ Invesco Asset Management (India) Private Limited does not warrant the completeness or accuracy of the information disclosed in this section and disclaims all liabilities, losses and damages arising out of the use of this information.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Share this article

|

Fund Focus: Invesco India Business Leaders Fund

Fund Focus: Invesco India Business Leaders Fund