|

|

|

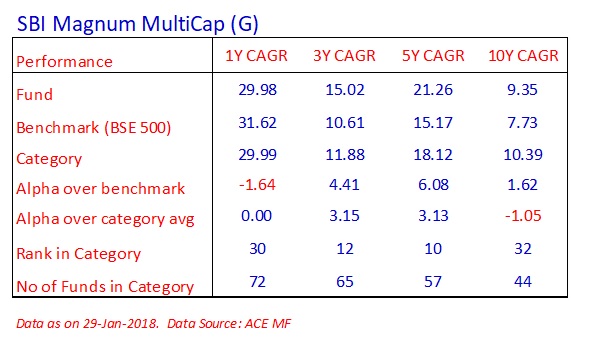

SBI’s MultiCap fund has been comfortably beating category averages over 3 and 5 year periods although the last 1 year has proved relatively more challenging. Anup discusses near term performance drivers, portfolio positioning, sectoral preferences and his overall take on whether markets are now trading in a bubble zone.

WF: Although your alpha over 3 and 5 years is commendable, the last year seems to have been more challenging. What are some of the inhibitors you faced recently in creating alpha and how are you overcoming them? Anup: The portfolio has grown faster than the average scheme in the Multicap category in the last 1 year, 6 months and 3 months. The last year was challenging for investors because of the unique and unprecedented event of demonetisation. The narrative of some of our stock positions were dependent on continued economic recovery. Such positions got beaten down after the announcement. We expected a deeper and more lasting impact of the event on real estate, financial services and discretionary consumption. The portfolio has recovered well since then. We have invested in stocks with good fundamentals, good growth outlook over the next 3 years. WF: How have you been aligning weights across large, mid and small caps in response to market dynamics? What have been the key changes in weights over the last 12 months? Anup: Our relative exposure to large caps, midcaps and small caps is a result of bottom-up stock picks. While we study the valuation and fundamentals of market cap-based indices, we don’t build the portfolio by taking top-down calls on large caps, midcaps or small caps. There is substantial diversity within stocks in every category. Our analysts study individual industries and stocks. They identify stocks that offer good growth outlook, clean corporate governance and that are available at attractive valuation. WF: How much flexibility does your fund mandate allow you in terms of weights across large, mid and small caps? Anup: We have sufficient flexibility to invest the fund in winners in every category. We can invest upto 10% of the fund in small-caps, between 10% to 40% of the fund in mid-caps and between 50% to 90% of the fund in large caps. WF: What have been the significant changes you have made at a sectoral / thematic level in your fund in the last 12 months and why? Anup: We have increased exposure to Telecom, IT and Construction sectors. Telecom sector has started consolidating. Many players like Telenor, RCOM, Aircel are in different stages of consolidation. This positive change led us to increase exposure to the sector. The IT sector has also started seeing some positive change at the margin with green shoots of higher discretionary spending by large clients. The construction sector has been benefitting from good order inflow, particularly in the roads segment. WF: Are we in bubble zone now at a broad market level? Where do you see dangerous bubbles building up? Anup: While investor sentiment is optimistic and valuation multiples are frothy in many stocks, it would be premature to conclude that the entire market is in a bubble zone. A bubble would be characterised by complete disconnect between ground reality and stock prices, surge in prices of stocks with no fundamental business story, surge in direct stock trading by retail investors etc. We don’t see widespread signs of these. Unfortunately, we are not allowed to comment on individual stocks in public media. Where do you see pockets of value in this rapidly rising market? Large cap IT and Pharma stocks can be said to be pockets of relative value in the current context. What do you see as the key risks today in the market? There has been increase in risk appetite in financial markets across the world. Credit spreads of low-rated corporate bonds, emerging market bonds and low volatility are some such signs. Negative news from Chinese financials sector or real estate, very sharp run-up in industrial commodities can trigger fall in risk appetite. This can lead to correction in global equity markets. India would also be impacted in such an eventuality. Secondary effect of GST implementation on unorganised, SMEs can possibly create negative news flow in India. However, we don’t expect such events in our base case. These are instances of possible risks. Share this article |

Fund Focus: SBI Magnum Multi Cap

Fund Focus: SBI Magnum Multi Cap