|

|

|

Balanced funds are no substitutes for bank FDs – they are inflation fighting solutions for investors who want relatively lower volatility in their equity exposures. With 70% in equity, you can’t expect zero volatility that you get with bank FDs. Just as important as managing this communication is the management of these funds as well says Srivatsa, who allocates a larger proportion of the equity component to large caps in the UTI Balanced Fund even as the debt exposure is more focused on accrual rather than duration strategies. Prudence in communication and in fund management are what Srivatsa stresses as pre-requisites for the burgeoning balanced funds category.

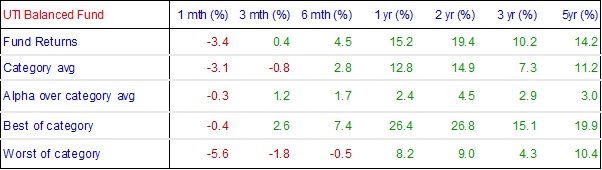

WF: What is at the core of the global market correction which is impacting our markets too? How deep a correction should we brace ourselves for? Srivatsa: I guess the signals of an impending global correction were reasonably evident over the last 3-6 months, as US treasury yields started climbing and liquidity at the margin began reducing. Perhaps some quant based selling accentuated the sell-off, however despite that, there was in fact a lot of complacency that had got into global markets over 2017 and this correction has served to take that away. The broad signal from global markets is that interest rates are in an up-cycle and when this happens, money does get re-allocated away from equity and into bonds. How deep a correction we should expect in India is difficult to say. Globally, money gets seamlessly re-allocated between asset classes depending on changing macro conditions. However, it doesn’t happen that way in India. Here, retail money does not move across asset classes. People may pause equity investing when they are concerned and then resume when nervousness reduces. Incremental retail flows into equity funds – which have been upwards of USD 3 billion a month, can perhaps reduce by a billion, but will still be very substantial. But money accumulated in equity in a SIP for example, does not move into debt funds when say the 10 yr G Sec yield breaches a certain threshold. WF: Many investors who have moved recently from FDs to balanced funds in the quest for higher returns are perhaps unprepared for corrections like what we are seeing. What should our messaging be to them today on the way forward for their investments? Srivatsa: What we have been articulating very clearly to our sales team and our channel partners is that balanced funds are not a replacement for bank FDs. Both have very different characteristics, composition and risk profiles. Merely because the 3 yr CAGR in balanced funds looks attractive, it does not make it a substitute for bank FDs. The year 2017 has seen historically low volatility and therefore investors who have been coming into balanced funds haven’t really experienced any form of volatility until now. We are now seeing a negative 1 month return after a very long period. But the fact remains that with a 70% exposure to equity, investors must expect bouts of volatility even as long term returns can continue to be comfortably higher than bank FD returns. Our message continues to be the same – invest in balanced funds as your first step towards equity investing, not as a substitute to bank FDs. Balanced funds are quasi-equity, the contain certain risk control mechanisms due to their 70-30 equity-debt allocation, which reduces but not eliminates volatility and yet enables the fund to deliver inflation beating returns in the long run. WF: In what ways are you finetuning the equity component of your balanced fund in light of the current gyrations in stock markets and concerns on rich valuations? Srivatsa: Over 70-80% of our incremental flows are being invested in the large caps space. Flows are healthy – in the last couple of months itself, we have got over Rs.700 crores in fresh inflows. As a philosophy, I adopt a value oriented strategy. So, even while we find mid and small caps at a category level expensive, I look for individual companies which continue to offer value. These could be a mid-cap IT company with robust growth prospects trading at a 30-40% discount to sector, or a cyclical where I am convinced about a turnaround and so on. In midcaps, I am completely bottom-up and to that extent am less worried about the overall valuations in that space. That said, in times of corrections like what we are seeing in the last few days, these stocks do come under pressure due to liquidity related issues – so one needs to be cautious about not overextending oneself in the midcaps space. So, out of the 70% net equity component, our aim is to have 50-55% in large caps and the balance 15-20% in midcaps. WF: What is your fixed income strategy in your balanced fund and how are you finetuning it in light of RBI’s policy stance? Srivatsa: The fixed income portion has always been more accrual focused and even within this strategy, we don’t venture into aggressive credit calls. UTI as you know, is known for its conservative stance on credit quality. Typically, around 70% of the fixed income component is accrual strategy oriented. The balance is in G-Secs where to a limited extent, duration strategies are adopted. Our view is that if rates inch up a bit more, that could be an attractive entry point into duration strategies. However, in this fund, we will typically not go beyond 40% of fixed income exposure into duration plays. We are conscious that investors in balanced funds expect relatively lower volatility than equity and see the debt portion as delivering that amount of stability. With these investor expectations, prudence suggests that we focus more on accrual than duration strategies in the debt portion. WF: Your balanced fund has been generating healthy alpha over category average across 1, 2 3 and 5 year horizons. What are some of the factors driving this performance? Srivatsa: Midcaps have been a good source of alpha for us and we have generally taken a longer term view in the midcaps space in our effort to create alpha. For example, we took a call last year in midcap IT companies when we saw growth returning and these stocks available at very reasonable valuations due to the overall depressed sentiment towards IT sector. We are currently overweight pharma and while this position hasn’t paid off yet, I am convinced that the inflection point is near and we will see healthy alpha coming in due to this allocation. So really, its about taking a slightly longer term view when taking positions in sectors and themes. Even in largecaps, we follow an active bets strategy. We continue to maintain zero exposure to some of the biggest market heavyweights where we are not convinced, even if this means a significant deviation from benchmark allocations to these big names. Likewise, we don’t hesitate to take significant overweight positions based on convictions in some of these index heavyweights. So, an active strategy in large caps coupled with a very sharp focus on stock picking in midcaps with a long term perspective is what has enabled us to deliver a healthy performance. Share this article |

Fund Focus: UTI Balanced Fund

Fund Focus: UTI Balanced Fund