|

GLOBAL

The US Federal Reserve, though it was not a unanimous decision, left interest rates untouched at its policy meeting in July. The current rate is in a target range of 0.25% - 0.50%. The central bank noted that the labor market had tightened, while the economy had progressed moderately. The Fed said that near term risks had lessened. The economy has handled the Brexit shock and the political uncertainties of a heated Presidential electoral season quite well. The Fed will meet again in September. "Information received since the Fed policy committee met in June indicates that the labor market strengthened and that economic activity has been expanding at a moderate rate," the Fed said. (RTT News July, 27, 2016)

Cautious optimism prevailed on the other side of the Atlantic as well. On Brexit, Mario Draghi, the President of the European Central Bank, ECB, said, "Following the UK referendum on EU membership, our assessment is that euro area financial markets have weathered the spike in uncertainty and volatility with encouraging resilience. Over the coming months when we have more information including new staff projections we'll be in a better position to assess the underlying macroeconomic conditions. What is clear is that financial markets and the banking sector have reacted in a fairly resilient fashion to the event. We haven't observed any disruption either in financial markets or the banking sector." (The Guardian, July, 21, 2016).

"The outcome of the UK vote, which surprised global financial markets, implies the materialization of an important downside risk for the world economy. As a result, the global outlook for 2016-17 has worsened, despite the better-than-expected performance in early 2016. This deterioration reflects the expected macroeconomic consequences of a sizable increase in uncertainty, including on the political front," the IMF said. (Livemint, July, 20, 2016)

NORTH AMERICA

US

ECONOMIC PERFORMANCE - In the second quarter, the US economy grew 1.2% year-on-year. This was better than the revised 0.8% growth posted in the previous quarter. However analysts were looking for a figure of 2.6%. Growth was propelled by a 4.2% surge in consumer spending, as also by the 1.4% growth in exports. The good performance was pulled down by declining contributions from state and federal governments, residential fixed investment, investment in inventories by private parties and non-residential fixed investment. Core inflation, stripped of food and energy prices, moved up 1.7% declining from the 2.1% posted in the previous quarter.

"The disappointing 1.2% annualized gain in second-quarter GDP growth, combined with the downward revisions to gains in the preceding two quarters, make a September interest rate hike much less likely," said Paul Ashworth, Chief U.S. Economist at Capital Economics."Over the past 12 months, the economy has expanded by only 1.2%," he added. "What is really worrying is that pace has still been enough to reduce the unemployment rate further, suggesting that the economy's potential growth rate could conceivably be close to zero."(RTT News, July 27, 2016)

CONSUMER SPENDING - Personal spending in the US inched up 0.4% in June, equaling the figure for May, while economists had expected a figure of 0.3%. Personal income increased 0.2%, less than growth of 0.3% analysts had predicted. Personal savings declined to 5.3% of personal income from 5.5% in May.

Personal consumption expenditures price index moved up 0.1% in June less than 0.2% increase witnessed in May. The annual increase was 0.9% in June. "Adding to the disappointing second-quarter GDP data, the lack of a clear pick-up in inflation will allow the Fed to delay the next rate hike until it has seen more concrete signs of a rebound in GDP growth, which all but rules out a September rate hike," Steve Murphy, U.S. economist at Capital Economics said. (RTT News, August 2, 2016)

MANUFACTURING ACTIVITY - US manufacturing activity declined in July. The Institute for Supply Management, ISM, reported that the Purchasing Managers Index, PMI had moved down from 53.2 in June to 52.6 in July. The index was pulled down by a fall in the employment index which measures employment in the manufacturing sector. The index dropped from 50.4 in June to 49.4. The prices index slumped from 60.5 in June, to 55.0 in July, while the supplier deliveries index nosedived from 55.4 to 51.8. New orders index dropped by 0.1 points. However, the production index increased from 54.7 to 55.4.

EUROPE

Eurozone

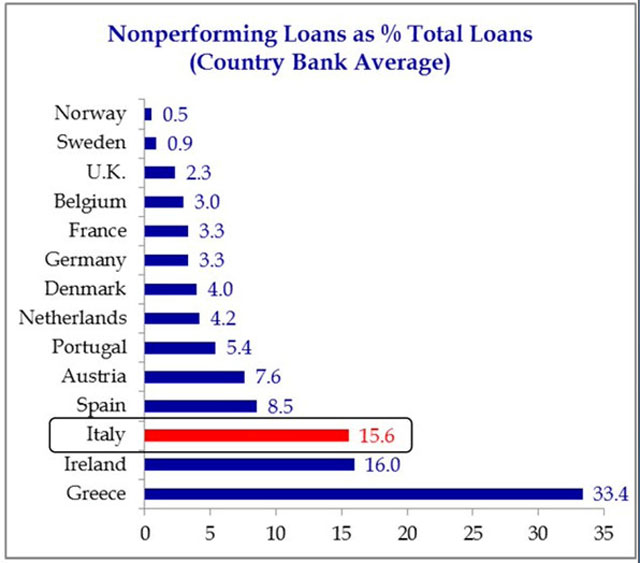

HEALTH OF BANKS - European Central Bank, ECB, President, Mario Draghi warned that non-performing loans were threatening the incipient economic recovery in the euro area. "The longer we have this (non-performing loan problem) in place, the less functioning will be the banking system, or at least will be the banks with high NPLs. And so the less capable will be these banks to transmit our monetary policy impulses to the real economy. Also, a high level of NPLs makes banks especially vulnerable to the markets." The ECB President insisted that the bank was ready to do all it can to contain the crisis in European banking. Economists say that the ECB will have to fine tune its policies to meet the new contingency. "In the past we've given enough evidence ... of our ability to adapt our purchases to reach 80 billion Euros a month until March 2017 or beyond."

This chart shows that Southern European countries need help the most:

Holger Zschaepitz

MANUFACTURING ACTIVITY - Economic activity in Europe slowed down slightly in July. According to Markit, the factory Purchasing Managers' Index, PMI, dropped to 52.0 in July from a half-year high of 52.8 in June. A reading above 50.0 signals expansion. This is 37th month of increase for the index. Slowing new orders was the most important factor in the decline.

The services PMI inched up to 52.9 in July after the seventeen month low of 52.8 witnessed in June. The composite index, which combines both, came in at 53.2 in July, the highest in six months, and more than the 52.8 reading in June. Economists were looking for a figure of 52.7 in July. According to Markit, "although the latest data signaled a solid and steady pace of expansion, national data suggested that the upturn was uneven by nation. Growth was primarily driven by an accelerated rate of output expansion in Germany, the fastest during the year-to-date. Rates of growth moderated in Italy and Spain, whereas France continued to hover around the stagnation mark."

GERMAN ECONOMY - Germany's factory PMI slid to 53.8 in July, from 54.5 in June, which was a 28 month high. Yet the index has expanded continuously for a year now. The services PMI was 54.4 in July, higher than the figure of 53.7 in June. The composite PMI surged to 55.3 in July, the highest in seven months, from 54.4 in June. "Germany's service sector continued to grow at the start of the third quarter with the underlying trend pace broadly in line with that seen over the past three years. Although new order growth also accelerated slightly from June's recent low, the rate of expansion was relatively mild, however," said, Oliver Kolodseike, an economist at Markit. (Financial Times, August, 3, 2016)

FRENCH ECONOMY - French manufacturing activity continued its downward path in July. The factory PMI inched up to 48.6 in July from 48.3 in June. Any reading below 50 shows a decline in output. In contrast, the services PMI for July pushed its way back to positive growth as the index grew to 50.5 in July from 49.9 in June. The composite PMI rose to 50.1 from 49.6. "Underpinning the renewed rise in service sector activity was a further increase in the level of new business received by French service providers. The latest rise in new work was the fifth in as many months and faster than that seen in June, albeit modest overall, according to Markit.

Jack Kennedy, a senior economist at Markit said France's services sector compensated "for ongoing manufacturing weakness, leaving overall private sector activity broadly flat on the month," but warned that: "Overall [there is] little sign of any change to the subdued pattern seen throughout the year to date. Indeed companies' business expectations remain at a historically muted level." (Financial Times, August, 3, 2016)

UK

CONSTRUCTION ACTIVITY - In July, the UK construction business dropped at the fastest rate in seven years. The Markit/Chartered Institute of Procurement & Supply Purchasing Managers' Index for the construction sector fell to 45.9 in July, from 46.0 in the previous month. Economists had forecast a figure of 44.0. Any reading below the 50.0 mark signals contraction. This is the second month the index is below the 50.0 mark. Slowing new orders dampened business in July, firms in the industry said. Employment in the sector too dropped, for the first time since 2013. The weaker sterling contributed to an increase in input costs. Further, uncertainties about private investment meant that confidence in the year-ahead business scenario was the lowest after April 2013.

BREXIT EFFECT ON MANUFACTURING - Confusion in the wake of the Brexit vote pulled down the manufacturing sector in the UK in July. Factory PMI was 48.2 in July tumbling from 52.4 in June. This is lowest reading since February 2013.A reading below 50.0 denotes contraction. Production dropped at the fastest pace since October 2012, while domestic demand remained weak. Employment sank at the quickest pace in more than three years and for the seventh month in a row; even as the slow inflow of new orders presage further declines. To make matters worse, input price increases were at a five year high due to the weak pound. In turn this pushed manufacturers to increase prices at the fastest pace in two years. However export orders witnessed growth, pushed by the weak sterling and efforts by manufacturers for overseas orders.

"The weakening order book trend and upswing in cost inflation point to further near-term pain for manufacturers," Markit Senior Economist Rob Dobson said."On that score, the weak numbers provide powerful arguments for swift policy action to avert the downturn becoming more embedded and help to hopefully play a part in restoring confidence and driving a swift recovery." (RTT News, August, 1, 2016).

ASIA

CHINA

CHINA MANUFACTURING - In July, the status of the Chinese manufacturing sector was confused as an official survey dropped into negative territory while, a private survey unexpectedly posted a gain for the first time in 17 months.

The official manufacturing PMI, that surveys government owned and large enterprises had a reading of 49.9, slightly lower than the reading of 50.0 in June. Economists had expected a figure of 50.0 in July too. The PMI had remained above the 50.0 mark from March until May, while the gauge had remained in negative territory for the earlier seven months. The private Caixin's PMI, which surveys small and medium private firms, shot up to 50.6 in July from 48.6 in the previous month. This is the first time since February 2015 that the index has climbed above the critical 50.0 mark. "Driving the headline index higher in July was a renewed rise in total new business. Though moderate, it was the first time that overall new orders had increased since March," Caixin said in its PMI report. (CNBC, July, 31, 2016).

The difference in the two surveys is attributed to the recent flooding in parts of China. This affected the regions where the large firms are located and whose activities have been disrupted in the short term, while smaller tech firms posted robust export sales. Yet the economy appears to be stabilizing after witnessing a period of increased capital outflows and depreciation in the value of the Yuan. The Chinese economy posted a growth of 6.7% on an annual basis in the second quarter. "(Caixin's) sub-indexes of output, new orders and inventory all surged past the neutral 50-point level that separates growth from decline. This indicates that the Chinese economy has begun to show signs of stabilizing due to the gradual implementation of proactive fiscal policy," said Zhengsheng Zhong, director of macroeconomic analysis at CEBM Group, a Caixin Insight Group subsidiary. "But the pressure on economic growth remains, and supportive fiscal and monetary policies must be continued," Zhong said.

The near-term outlook of China has improved due to recent policy support, IMF said. "China's growth outlook is broadly unchanged relative to April (with a slight upward revision for 2016). However, should growth in the European Union be affected significantly, the adverse effect on China could be material," it added. (Livemint, July, 20, 2016)

JAPAN

CONSUMER CONFIDENCE - The July consumer confidence index in Japan witnessed an unforeseen fall. The index dropped from 41.8 in June to 41.3 in July, even as economists forecast an increase to 42.0. The reading in June had been the highest for five months. The index for willingness to buy durable goods worsened from 42.1 in June to 41.3 in July. The employment index slid to 43.7. The index for income growth moved down from 41.4 to 40.7.

SOUTH KOREA

TRADE BALANCE - Exports declined in July in South Korea, continuing the trend of the last 19 months, the Ministry of Trade, Industries and Energy said. Exports slumped 10.2% year-on-year to $41.05 billion in July, while exports had fallen 2.7% in June. Analysts were looking for a decline of 7% in July. Imports tumbled 14.0% on an annual basis to $33.25 billion, while economists had expected a fall of 9.5%. The July trade surplus was $7.79 billion, less than the surplus of $11.50 billion in the previous month. In export dependent South Korea, exports have been declining for the last year and a half, caused by slowing global trade, economic slowdown in China and low oil prices.

This data shows that the South Korean economy continues to face strong headwinds, while having to deal with increasing Chinese competition in its traditional technology focused industries. According to Gareth Leather, senior Asia economist at Capital Economics, there are fears that a far wider range of Korean exporters could be hit as China continues to develop its manufacturing prowess. "So far, it has been mostly Korea's electronics companies that have suffered, but this could start to change," he warns. "Chinese car companies have been doing well in emerging markets, and could soon start to gain market share from Korean companies. China is also rapidly gaining market share in the shipbuilding industry. In recent years it has gained market share at the expense of shipbuilders from Japan, and recently overtook Korea as the world's biggest shipbuilder," he said.

INDIA

ECONOMIC GROWTH - The Nikkei/Markit Services Purchasing Managers' Index soared to 51.9 in July, from 50.3 in June. This is the thirteenth consecutive month for which the index has been above the 50.0 mark. The new business sub-index grew strongly to 51.7 in July, from 50.5 in the earlier month. However firms had to cut prices, the first time since October. This trend could help contain inflation and prod the Reserve Bank of India, RBI, to continue its cycle of easing. Inflation was 5.77% in June, above the RBI's target of 5%. The factory PMI too, pushed by exports, increased. The Composite PMI, including both manufacturing and services, moved up to 52.4 in July, from 51.1 in June. "The Indian service economy started the second semester on a solid footing, posting its strongest performance since April and thereby indicating that underlying demand conditions remained reasonably firm," said Pollyanna De Lima, economist at survey compiler Markit.

GROWTH PROSPECTS - The Confederation of Indian Industry's Business Outlook survey revealed that a majority of firms had placed investment plans on hold, despite expectations of improved sales. A stagnant economy, combined with existing unutilized capacity, has made 49.7% of the firms to keep their domestic investment plans on hold. Fully 60.5% of the firms have shelved international investment plans given the confused global economic situation.

The IMF revised the growth forecast to 7.4% from the earlier 7.5% for the fiscal year 2016-2017. "In India, economic activity remains buoyant, but the growth forecast for 2016-17 was trimmed slightly, reflecting a more sluggish investment recovery," IMF said in an update to its World Economic Outlook. India's economy grew at 7.6% in 2015-2016 and the government has targeted 8% in the current fiscal year.

The salary hike of about 24% for government employees is likely to stoke consumer spending. Likewise a strong monsoon is expected to lift up agricultural fortunes. According to the Asian Development Bank, ADB, there are several positives to the economy now. "The improved monsoon encouraged more planting of rice, pulses and sugarcane into July. There are some signs of an uptick in rural demand in anticipation of good monsoon and a rural-oriented government budget. Reforms like the passage of the Bankruptcy Code, which creates time-bound processes for resolving corporate insolvency, and the easing of rules governing foreign direct investment are likely to facilitate business," it added. (Livemint, July, 20, 2016).

Share this article

|

Current Conversations: Sound Bytes

Current Conversations: Sound Bytes