|

WF: In your presentation, you have talked about similarities of the current period with earlier trends in the 90s and 00s and have talked about a 5/5 score on your equity score card. Can you please elaborate on these perspectives?

Lalit: Lets take the two issues separately - the first relates to similarities with earlier periods and the second is about the equity score card.

If you look historically, markets are generally driven by the combination by PE expansion and followed by earnings growth. For a sustained upswing or rally, both these components are required and a rally led by either one of them individually does not sustain. PE expansion is usually a function of sentiments, emotions and expectations. We saw this in India in 2014 in the election results euphoria and in the 1990s post liberalisation. Expectations were very high and that led to a PE expansion. In the early 2000s, post 9/11, the US Fed took swift action that unleashed liquidity into global markets and brought on a risk on trade that resulted in PE expansion across the globe. In all three situations, there was a lull after the initial PE expansion led rally, as EPS growth did not happen immediately thereafter. We saw that in the earlier two decades and we saw that in 2015 and 2016 as well. The other similarity between now and the periods mentioned in the last 2 decades is that in all three situations, inflation bottomed out and credit growth also bottomed out. This sets the stage for a meaningful recovery.

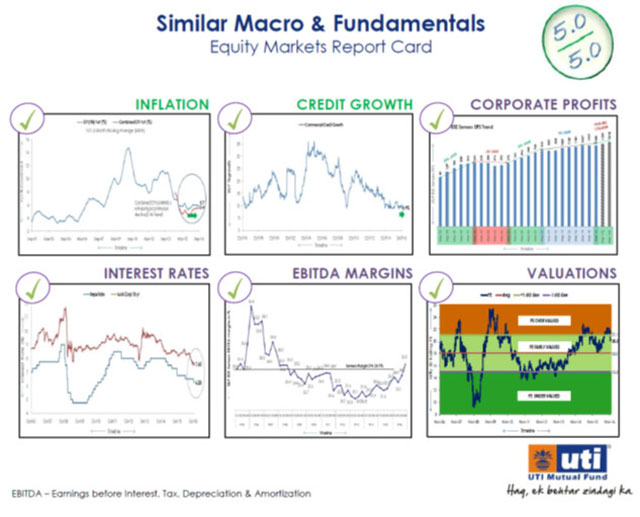

Now coming to our equity scorecard which we have been running for 2 years now, we track 5 key parameters which we believe are good pointers to where markets can head in the future as these have historically been proven to be key market drivers. These are inflation, interest rates, credit growth, corporate profits (with EBIDTA margins as a key driver within corporate profits) and valuations. We believe inflation, has bottomed out, interest rates are bottoming out, credit growth and corporate profits have bottomed out and valuations - though not bottoming out, are in fair value zone.

What this means is that the stage is set for a meaningful equity market rally driven by earnings expansion to take place. However, it does not follow that we will see a V shaped rally - it is more likely to be a U shaped one.

WF: Why do you believe domestic facing cyclicals is the sweet spot to invest in today?

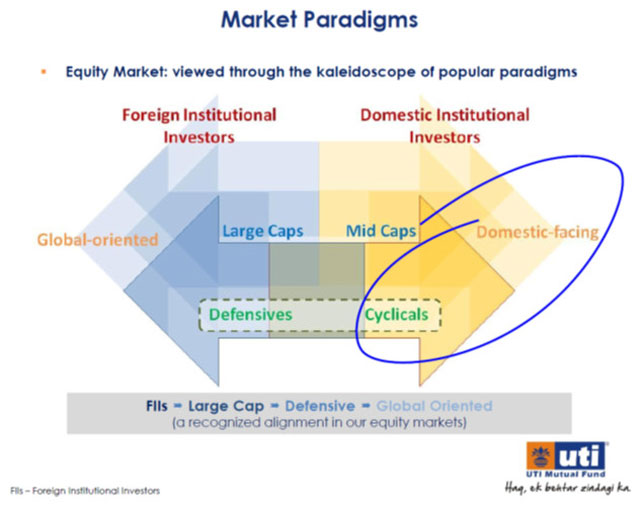

Lalit: The chart below aptly summarizes the key market paradigms in terms of the main players and the typical market segments that they lean more towards.

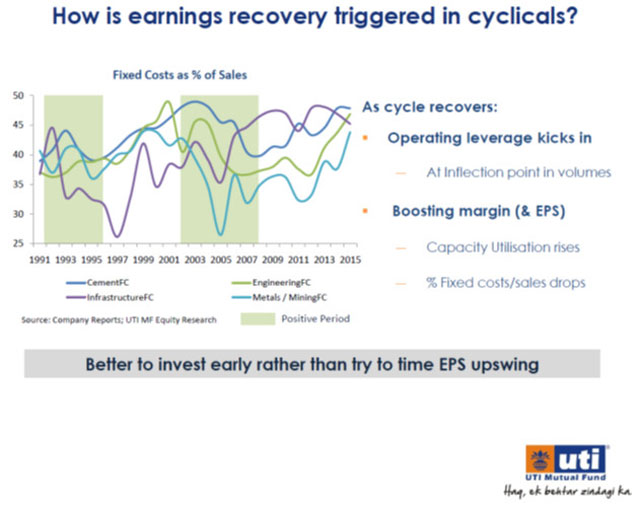

Domestic facing cyclicals is one segment of the market that is under-owned and has been least talked about in recent times. It is under-owned because this is the segment that has seen maximum profitability strain in the years following the 2008 meltdown. They had invested in huge capacity expansion prior to the crash and then volumes never came through to support this incremental fixed cost, which meant that their fixed cost as a %age of sales rose to very high levels, thus impacting profits, as can be seen in this chart.

As volumes grow in an economic recovery phase, operating leverage kicks in most for these companies, their fixed cost as a %age of sales declines considerably, and earnings growth starts galloping upwards. Our key investment thesis is that it is better to invest early in this segment, ahead of the expected earnings upswing, rather than trying to time an entry to perfection, just when the upswing has taken firm root. We know that private sector capex hasn't yet taken off in a material way. Nobody can pinpoint exactly when the inflection point will be crossed, but we know it is imminent. Its best to prepare your portfolios for the next wave rather than trying to crest it at exactly the right time.

If you look at the last two decades, in both cases, domestic cyclicals came into a sweet spot with conditions that are similar to what we see now, and then they led the market rally in the subsequent years on the back of robust earnings expansion. Our sense is that this is again that once-in-a-decade opportunity to ride the domestic cyclicals theme in the years ahead.

WF: You talked about the much delayed private sector capex revival: you have made an observation in your presentation that conditions were never better in the last 8 years. Can you please elaborate on this?

Lalit: The biggest driver for private sector capex revival is capacity utilization - higher utilization levels fuel more capacity expansion. Our understanding from RBI is that the current utilization levels are around 72% and the lowest have been around 70%. One way to look at it is that we are still far off from a sustained private sector capex revival.

But the reality is a little different. In reality, revival doesn't happen with all entrepreneurs jumping into the action together. There are many who will be on the sidelines and some who will start investing in capacity expansion, to stay ahead of the curve, to capture the most of the demand revival because they will be the ones with higher capacity already in place. We are seeing a lot of evidence of individual businesses doing this right now - we see a couple of cement companies who have embarked on capacity expansion, we are seeing a pharma major doing this, a leading food brand doing this, a leading fertilizer player is expanding capacity and even unlisted majors like Amul who are expanding capacity to cater to future growth.

These are not big steel and power plants that materially move the needle at a macro level. But these are numerous incremental steps taken by diverse companies, which is happening as we speak. So, optically it might appear that the needle hasn't moved much, but you dig deeper and go bottom up, and you will find encouraging signs - which means one has to think seriously about how to catch this trend early on - before the headline numbers start demonstrating that the wave is well and truly underway. There are enough first movers right now who are expanding capacity ahead of the curve - our job is to track these and spot good investment opportunities in them - ahead of the curve.

Why we say that conditions have not been better than now in the last 8 years is that all the drivers for private sector capex are now falling into place: interest rates are heading down, cost of capital is therefore falling, banks are now eager to lend - having seen through the worst of the stressed assets problems, Government capex momentum is strong, large corporates have seen through some painful deleveraging and have better balance sheets now. So, the stage is set, in our view, for a broad based private sector capex revival.

WF: To what extent do you see demonetization and GST implementation impacting domestic cyclicals from a near and medium term perspective?

Lalit: For domestic cyclicals specifically, the impact I believe is neutral to positive in the medium term. Large sections of domestic cyclicals are B-2-B, which are not impacted much by demonetization, and which will be positively impacted by GST implementation.

That said, I do believe that the negative impact of demonetization on the market as a whole is perhaps overblown. If all the money has indeed come back into the system (which is being pointed out as a key failure of demonetization), then where is the negative medium term impact?

On GST implementation, the sense I get when I speak with a lot of people is that it might get delayed. There may not be appetite for two back-to-back disruptions in the form of GST implementation coming close on the heels of demonetization.

WF: What will be the likely proportion of large and midcaps in your initial portfolio?

Lalit: There are not too many large cap players in the domestic cyclicals theme - so the portfolio is likely to have a midcap bias. We don't have fixed numbers in mind, but I would believe there will be a larger proportion of midcap stocks in this portfolio.

WF: Are you likely to look for ongoing profit booking in an attempt to pay out regular dividends from this closed ended fund or will you be more inclined to a buy and hold strategy?

Lalit: No, we are not contemplating an active profit booking strategy in this fund. We believe the best way to play this theme is to get in early - get in ahead of the curve, and then ride it fully through the cycle. For this reason, although it is an ELSS fund, we have opted for a 3+7 structure. The first 3 years are locked in due to the tax break related regulations. After 3 years, investors can stay invested for a further 7 years and can redeem at any stage in this subsequent 7 year period. We don't take in money after 3 years - it is closed ended from that point of view.

WF: What will you say is the key investment argument for this fund at this point in time?

Lalit: This is a once-in-a-decade investment opportunity in our view. This is a pure play on domestic cyclicals. It is a pure play on the economic cycle. There aren't too many such funds in the market. Our belief is that now is the time to make a focused investment in domestic cyclicals - get in ahead of the curve and ride the entire curve. Don't try to time it - but harness its full potential. This is a fund that enables you to do this, even as it provides you a tax break that ELSS funds do.

Share this article

|

AMC Speak

AMC Speak